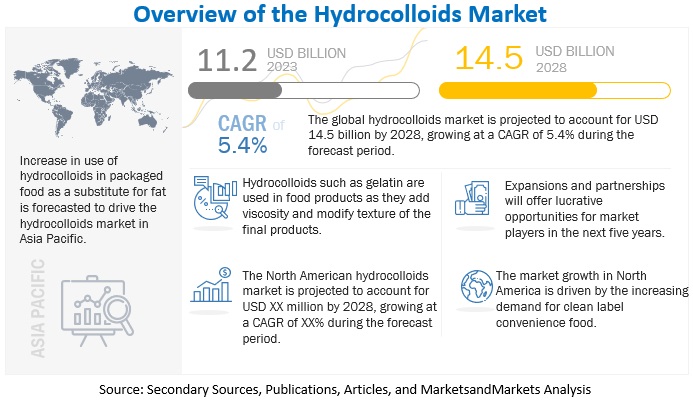

The hydrocolloids market refers to the industry involved in the production and distribution of hydrocolloids, which are a group of substances that can form a gel-like structure when combined with water. These compounds are widely used in various industries, including food and beverages, pharmaceuticals, cosmetics, and more.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1231

Hydrocolloids play a crucial role in food products, where they are used as thickening agents, stabilizers, emulsifiers, and gelling agents. Common examples of hydrocolloids include carrageenan, guar gum, xanthan gum, pectin, and agar. These ingredients contribute to the texture, viscosity, and overall quality of many processed foods.

The food industry represents a significant portion of the hydrocolloids market, driven by the increasing demand for processed and convenience foods. Hydrocolloids are essential in enhancing the sensory attributes of food products and improving their shelf life. Additionally, they are employed in the pharmaceutical industry for various purposes, such as the formulation of drug delivery systems.

The cosmetics and personal care industry also utilize hydrocolloids in the production of creams, lotions, and other beauty products. Their ability to modify the rheological properties of formulations makes them valuable in achieving the desired texture and stability in cosmetic applications.

The market for hydrocolloids is influenced by factors such as consumer preferences for convenience foods, the growing awareness of health and wellness, and advancements in food technology. As the demand for innovative and functional ingredients continues to rise, the hydrocolloids market is expected to experience sustained growth.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1231

Manufacturers in the hydrocolloids industry focus on research and development to discover new applications and improve the functionality of existing hydrocolloid products. This constant innovation contributes to the expansion of the market and provides opportunities for businesses to meet evolving consumer demands.

Overall, the hydrocolloids market plays a vital role in various industries, offering versatile solutions for product development and formulation across food, pharmaceuticals, cosmetics, and other sectors. The ongoing evolution of consumer preferences and industry regulations will likely shape the trajectory of this market in the coming years.