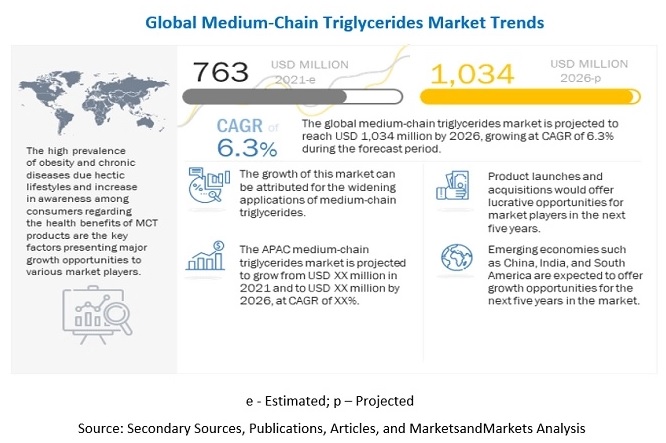

The Medium Chain Triglycerides (MCT) market is set to experience robust growth, with a projected CAGR of 6.3% between 2021 and 2026, culminating in a market value of $1,034 million by 2026 from an estimated $763 million in 2021. The increasing preference for organic food products has prompted MCT manufacturers to focus on innovative, cost-effective solutions, while the surge in global Internet penetration is expected to drive sales.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248063458

Caprylic Acid Segment Takes Center Stage

The caprylic acid segment has emerged as a dominant force in the market, claiming an impressive 50.4% share in terms of value. Recognized for its neutral taste and odor, caprylic acid is a key component in MCT oil. Beyond culinary applications, caprylic acid boasts antiviral, antibacterial, and antifungal properties, addressing skin disorders, acne, urinary tract infections, and more. Its rapid oxidation in the liver contributes to increased energy expenditure, making it a versatile compound.

Nutritional Supplements Lead Application Segment

The nutritional supplements segment commands a substantial share of 25.9%, totaling USD 186.5 million. Medium chain triglycerides play a pivotal role in weight management by curbing calorie intake, reducing fat storage, and enhancing fullness, calorie burning, and ketone levels, particularly in low-carb diets.

Health Benefits Drive Market Momentum

Medium chain triglycerides offer a range of health benefits, from improved weight management to enhanced cognitive functioning. Their rapid digestion, minimal storage as body fat, and contribution to heightened metabolism position them as a triple approach to weight loss. Additionally, MCTs support gut health and are linked to reduced risks associated with hormone imbalances, weight gain, gut problems, and cognitive disorders.

China Leads Asia Pacific Market

China dominates the Asia Pacific market, boasting a 31.1% share in 2020, establishing itself as a rapidly growing market within the region. Evolving consumer lifestyles, increased purchasing power, and a growing demand for high-quality processed foods, nutritional diets, personal care, and cosmetics products contribute to the surge in MCT demand. The rise in chronic diseases, as reported by the WHO, further propels the market for functional food ingredients.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=248063458

Key Players Shaping the Industry

Key players in the Medium Chain Triglycerides market include BASF SE (Germany), Koninklijke DSM N.V. (the Netherlands), Dupont (US), Lonza Group Ltd (Switzerland), Musim Mas Holdings (Singapore), Croda International Plc (UK), P&G Chemicals (US), Acme-Hardesty Company (Bluebell, PA), Wilmar International Limited (Singapore), Stepan Company (US), Sternchemie GmbH & Co. KG (Germany), Emery Oleochemicals Group (US), KLK Oleo (Malaysia), Nutricia (New Zealand), Connoils (US), Now foods (US), Barleans (Washington), Jarrow formula’s (US), Nutiva (US), Henry Lamotte Oils GmbH (Germany).