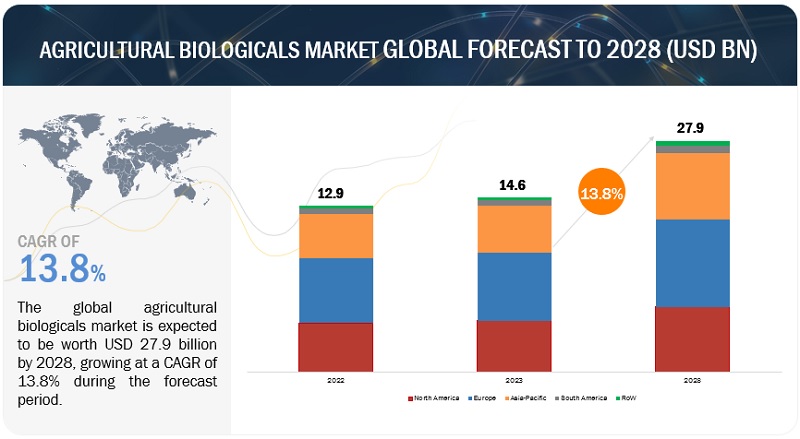

The agricultural biologicals market size is anticipated to reach USD 27.9 billion by 2028 from USD 14.6 billion in 2023, at a CAGR of 13.8% during the forecast period in terms of value. Stricter regulations enforced by governments and regulatory bodies globally aim to safeguard human health and the environment by limiting the use of chemical pesticides. Consequently, there is a growing demand for safer and more sustainable alternatives, driving the increased adoption of agricultural biologicals across the globe.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=100393324

Agricultural Biologicals Market Driver: Stricter Regulations Drive Adoption of Agricultural Biologicals as Sustainable Pesticide Alternatives

Governments and regulatory bodies around the world are increasingly recognizing the potential risks associated with chemical pesticides. These risks include adverse effects on human health, such as pesticide residue on food, as well as environmental concerns, such as contamination of water sources and harm to non-target organisms like beneficial insects and wildlife. To address these concerns, stricter regulations are being implemented to mitigate the use and impact of chemical pesticides.

This regulatory shift has prompted a significant shift in the agricultural industry, with an increasing demand for safer and more sustainable alternatives to conventional chemical pesticides. This demand has led to the rise of agricultural biologicals as viable solutions.

Agricultural Biologicals Market Opportunity: The Rise of Integrated Pest Management: Driving Opportunities for Agricultural Biologicals

Integrated Pest Management (IPM) is gaining global recognition as a holistic approach that combines diverse pest control strategies, including biological control methods. Within the realm of IPM, agricultural biologicals play a crucial role in promoting sustainable pest management practices and reducing reliance on chemical pesticides. As the adoption of IPM practices continues to increase worldwide, it presents significant opportunities for the utilization of agricultural biologicals across diverse cropping systems. By integrating biological control agents, such as beneficial insects, microbial-based products, and plant extracts, into IPM strategies, farmers can effectively manage pests while minimizing negative impacts on the environment and human health.

Strict regulations to drive the demand for the agricultural biologicals market

The European Union (EU) has taken a leading role in implementing strict regulations on chemical pesticides. Through the Sustainable Use Directive (2009/128/EC), the EU promotes integrated pest management (IPM) practices and encourages the utilization of non-chemical methods, including biological controls. As a result, there has been a substantial reduction in the use of chemical pesticides within European agriculture, with an increased adoption of agricultural biologicals.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=100393324

North America is expected to dominate the market during the forecast period

The global agricultural biologicals industry has seen significant growth in North America, primarily due to the high level of awareness and willingness among farmers in the United States and Canada to adopt sustainable agricultural practices. Farmers in these regions have recognized the increasing demand for organic and sustainable food, as well as the concerns surrounding chemical pesticide use. Consequently, they have actively sought alternatives such as agricultural biologicals, which has fueled market growth.

North America also benefits from well-established distribution networks and marketing channels for agricultural inputs. The presence of established agricultural input suppliers, including distributors and retailers, has played a crucial role in making agricultural biologicals easily accessible and readily available to farmers. This streamlined distribution system has further facilitated the growth of the agricultural biologicals market in the region.