Introduction:

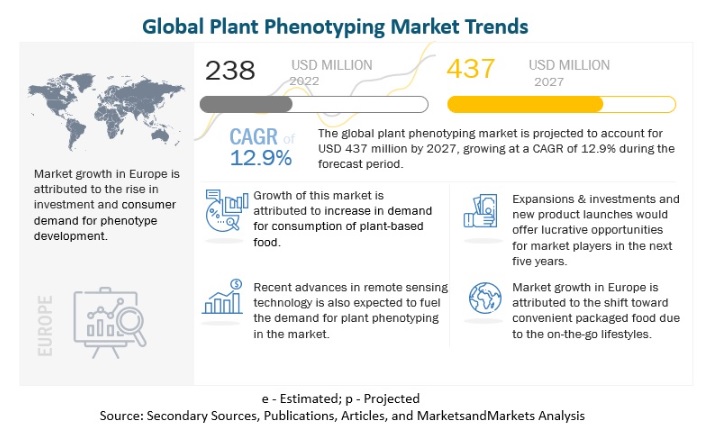

The global plant phenotyping market is on a trajectory to reach a staggering USD 437 million by 2027, showcasing a robust Compound Annual Growth Rate (CAGR) of 12.9% during the forecast period. This meteoric rise is propelled by a confluence of factors, including burgeoning expansions and investments in plant phenotyping within developed regions. Notably, the market is experiencing a surge due to the escalating importance of sustainable crop production through the cultivation of improved crop varieties.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=236591018

Factors Driving Growth:

Expansions and Investments:

Increasing expansions and investments in plant phenotyping, particularly in developed regions, stand as a pivotal driver for the market’s growth. This trend underscores the industry’s commitment to advancing agricultural practices through cutting-edge technology.

Emphasis on Sustainable Crop Production:

The growing emphasis on sustainable crop production, achieved through the cultivation of enhanced crop varieties, serves as another significant factor fueling the expansion of the plant phenotyping market. This shift reflects a broader commitment to environmentally conscious agricultural practices.

Government Funding and Support:

Europe and North America have witnessed a surge in government and organizational funding for plant phenotyping experiments. This financial backing has played a pivotal role in propelling the market’s growth, fostering innovation and research in these regions.

Regional Dynamics:

Europe and North America:

High levels of government funding for plant phenotyping experiments in Europe and North America have been instrumental in driving market growth. These regions serve as hubs for innovation, with a focus on advancing agricultural practices through technology and research.

Asia Pacific:

Developing countries in the Asia Pacific region are emerging as significant players in the plant phenotyping market. The demand for plant phenotyping products and services in these countries is driven by the need to address challenges related to food, fuel, and feed demand for their growing populations. Additionally, the development of plants capable of withstanding changing climatic conditions is a key driver in the region.

Key Players:

Leading the charge in the plant phenotyping market are key companies involved in both product manufacturing and service provision. Notable names include LemnaTec GmbH, Delta-T Devices Ltd., CropDesign – BASF SE, Heinz Walz GmbH, Phenospex B.V., WPS, Phenomix, Photon Systems Instruments, Qubit Systems, KeyGene N.V., Rothamsted Research Limited, The Vienna Biocenter Core Facilities GmbH (VBCF), and Equinom.

Request for Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=236591018

Technological Advancements:

In response to the growing demand for sophisticated applications, companies in the plant phenotyping market are continuously advancing their products and services. A significant development lies in the image analysis segment, projected to account for the largest share in 2022. These standalone or additional accessories, integrated into plant phenotyping equipment systems, demonstrate the industry’s commitment to cutting-edge spectrometry and imagery techniques.

Conclusion:

The global plant phenotyping market is not just witnessing growth; it’s undergoing a transformative journey fueled by innovation, sustainability, and a global commitment to revolutionize agricultural practices. As expansions, technological advancements, and regional dynamics shape the landscape, the market is poised to play a pivotal role in addressing the evolving challenges of our agricultural future.