According to the US Farm Bill 2014, industrial hemp is defined as, “the plant Cannabis sativa L. and any part of such plant, whether growing or not, with a delta-9 tetrahydrocannabinol (THC) concentration of not more than 0.3% on a dry weight basis.”

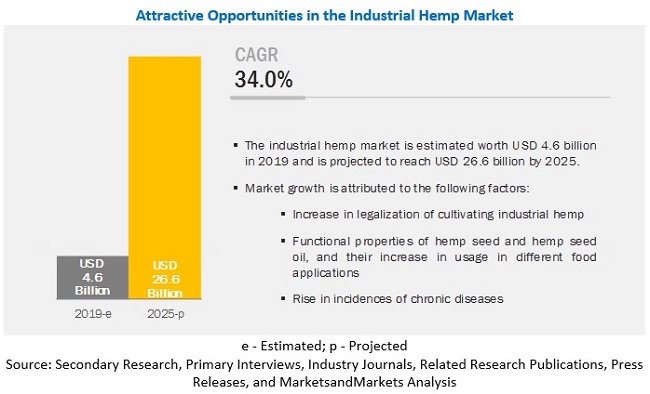

MarketsandMarkets projects that the global industrial hemp market is projected to grow from USD 4.6 billion in 2019 to USD 26.6 billion by 2025, recording a compound annual growth rate (CAGR) of 34.0% during the forecast period. The growing usage of hemp-derived seed as a superfood due to its rich nutritional profile and other health benefits is driving the market for industrial hemp. Furthermore, increasing legalization of hemp in different countries across the world is also driving the growth of industrial hemp.

Download PDF brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=84188417

Hemp fiber is estimated to dominate the market for industrial hemp in 2019. It is used primarily in the textile and pulp & paper industry, due to its long and robust fibers as compared to cotton. Furthermore, being a renewable source material, its application to obtain biofuels and bioplastics has been expected to increase its demand in the coming years.

Food is projected to be the dominating application segment of the industrial hemp market during the forecast period due to the wide application of hemp seeds and hemp seed oil in food products for their vitamins, proteins, and omega-3 fatty acid content. Hemp seeds are consumed raw or are used as a topping in cereals, smoothies, and yogurt. Rising consumer awareness about the benefits of consuming hemp-based products is driving the market for its application in food.

In terms of geographic coverage, the industrial hemp market has been segmented into four regions, namely, North America, Europe, Asia Pacific, and Rest of the World (RoW). Europe is projected to be the fastest-growing region during the forecast period owing to growth in consumption of hemp seeds as food as well as their broad application in other food products such as smoothies, yogurt, cereals, and bars especially in countries such as Germany and the Netherlands. Moreover, the rise in awareness among consumers about the nutritional benefits of consuming hemp is further expected to fuel the demand for hemp-based food and personal care products. Furthermore, increasing legalization of industrial hemp in the European region in the coming years is expected to boost the industrial hemp market.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=84188417

The increasing legalization of the cultivation of hemp provides enormous opportunities to the manufacturers and research institutions to develop new products from industrial hemp. Bioplastic is one such product that can be manufactured from the leftover of hemp seeds and CBD oil. Furthermore, biofuel derived from the hemp plant provides opportunities for the companies to explore this application of hemp as a fuel for automobiles. The growing consumer demand for sustainable goods, along with initiatives and support from corporate and government, is expected to support the growth of hemp-based biofuel and bioplastics in the coming years.