According to MarketsandMarkets, the global bakery premixes market size is estimated to be valued at USD 298 millionin 2019 and is projected to reach USD 413 millionby 2025, recording a CAGR of 5.6% from 2019to 2025. Theincreasing number of product launches from major companies and the rising demand for quick and convenient baking solutionsare some of the factors driving the growth of the bakery premixes market.

Thebakery premixesmarket isprojected to witness high growth due to the increasing global population in developing countries and the rising bakery consumption across the globe. The busy lifestyles and increasing consumer inclination toward convenience food products are factors that have also led to a risein demand for bakery products.

Currently, the key players in the market are focusing on launching new types of bakery premixes,such as Oy Karl Fazer AB(Finland),Archer Daniels Midland Company(US),Cargill(US),Corbion(Netherlands),and Bakels Group(Switzerland).These companies provide high-quality bakery mixes across the globe.The primary focus of these companies is to launch new products, which helps it integrate and diversify its product portfolio.

Request for Customization of the Report: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=126304017

Complete mix is one of the major categories in the bakery premixes market, which is projected to witness significant growth during the forecast period, due to the high convenience associated with usage of the complete mix. The major advantage associated with complete mix is convenience, as only water is added to the product. Complete mixes are the type of bakery premixes that are used as readymade mixtures based on rye flour, wheat for making bread, and other bakery products such as pastry, mixes, and pancakes.

The bakery products segment is projected to dominate the bakery premixes market share during the forecast period. This is due to the increasing application of premixes in bakery products, such as pastries, cakes, muffins, donuts, and pancakes. In addition, the bread products segment is projected to record high growth in the coming years. This is due to the increasing trend of consuming bread products, which drives the demand for bread premixes.Thecakes subsegment is projected to account for the largest share in the market, as cake mixes are convenient to use and provide a moist texture and consistent flavor to the final products. These products are available in different flavors, such as chocolate, vanilla, and fruits, which is projected to drive the growth of the bakery premixesmarket over the forecast period.

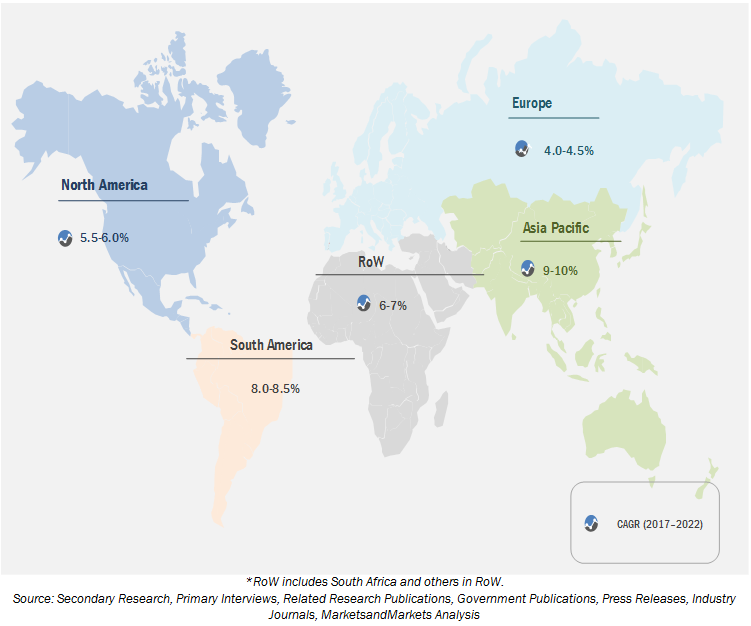

The South Americanbakery premixes market is projected to offer high growth potential in the coming years. The region includes countries such as Brazil, Argentina, Peru, Chile, Colombia, Uruguay, Ecuador, and Venezuela. These countries are witnessing a significant increase in consumption of on-the-go food products due to the adoption of urbanized lifestyles among consumers. This has encouraged consumers to opt for on-the-go food options, which has led to high demand for bakery products among consumers in the region. The expansion of supermarket chains and convenient stores has further led to a rise in sales of bakery products in the region, as theyare fast occupying supermarket shelves.