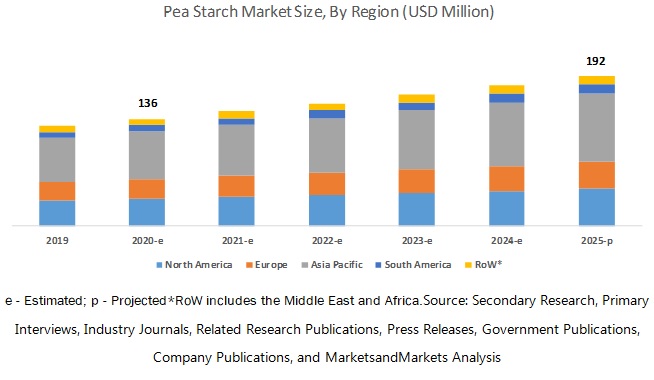

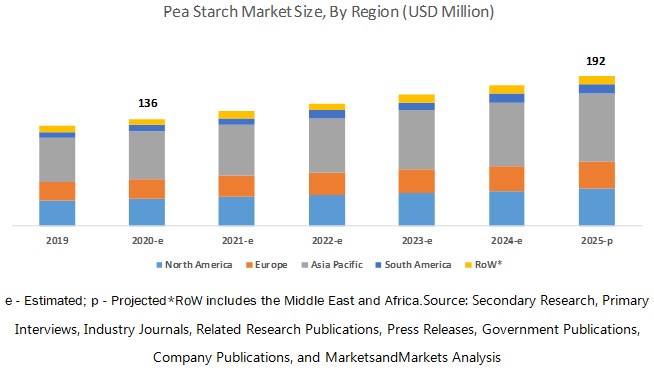

The pea starch market is projected to grow from USD 136 million in 2020 to USD 192 million by 2025, recording a compound annual growth rate (CAGR) of 7.0% during the forecast period. The major factors driving the growth of the pea starch market include the rise in the consumption of clean label convenience products, the increase in demand for gluten-free products among consumers, and the growth of economies that enable high acceptance of these products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=78961382

Drivers

- Growth In Demand For Pea Starch From Various End-Use Industries

- Increase In Demand For Gluten-Free Food Products

- Cost-Effectiveness Of Manufacturing Pea Starch

Restraints

- Effect Of Retrogradation On The Functional Properties Of Pea Starch

- Decrease In The Production Of Dry Pea

Opportunities

- Rising Demand From The Pet Food Industry

Challenges

- International And Domestic Food Safety Standards

- Threat Of Substitute Starches

- Trade Barriers Due To Covid-19 Outbreak

The food segment is projected to account for the largest share in the pea starch market, followed by the feed segment during the forecast period.

Pea starch provides a gluten-free, allergen-free, low-calorie, low-fat solution to food manufacturers. It also helps in enhancing the texture, consistency, and quality of food products. Moreover, the trends of clean label and gluten-free products are increasing. These trends are projected to favor the growth of pea starch market.

Request for Sample Report Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=78961382

The Asia Pacific region is projected to be the fastest-growing market for pea starch during the forecast period.

The Asia Pacific region is projected to be the fastest-growing market for pea starch during the forecast period. Asia is among the largest pea processing regions in the world. The growing disposable incomes and appetites for convenience and comfort in a fast-paced, urbanized world have caused a serious growth in the consumption of processed food products. This will lead to the growth of the pea starch market in the region as pea starch helps in enhancing the quality of processed food products.

Key players in the global pea starch market include Emsland Group (Germany), Ingredion Incorporated (US), Cosucra Groupe Warconing (Belgium), Roquette Frères (France), Axiom Foods (US), and Yantai Shuangta Food (China). These players have broad industry coverage and high operational and financial strength.