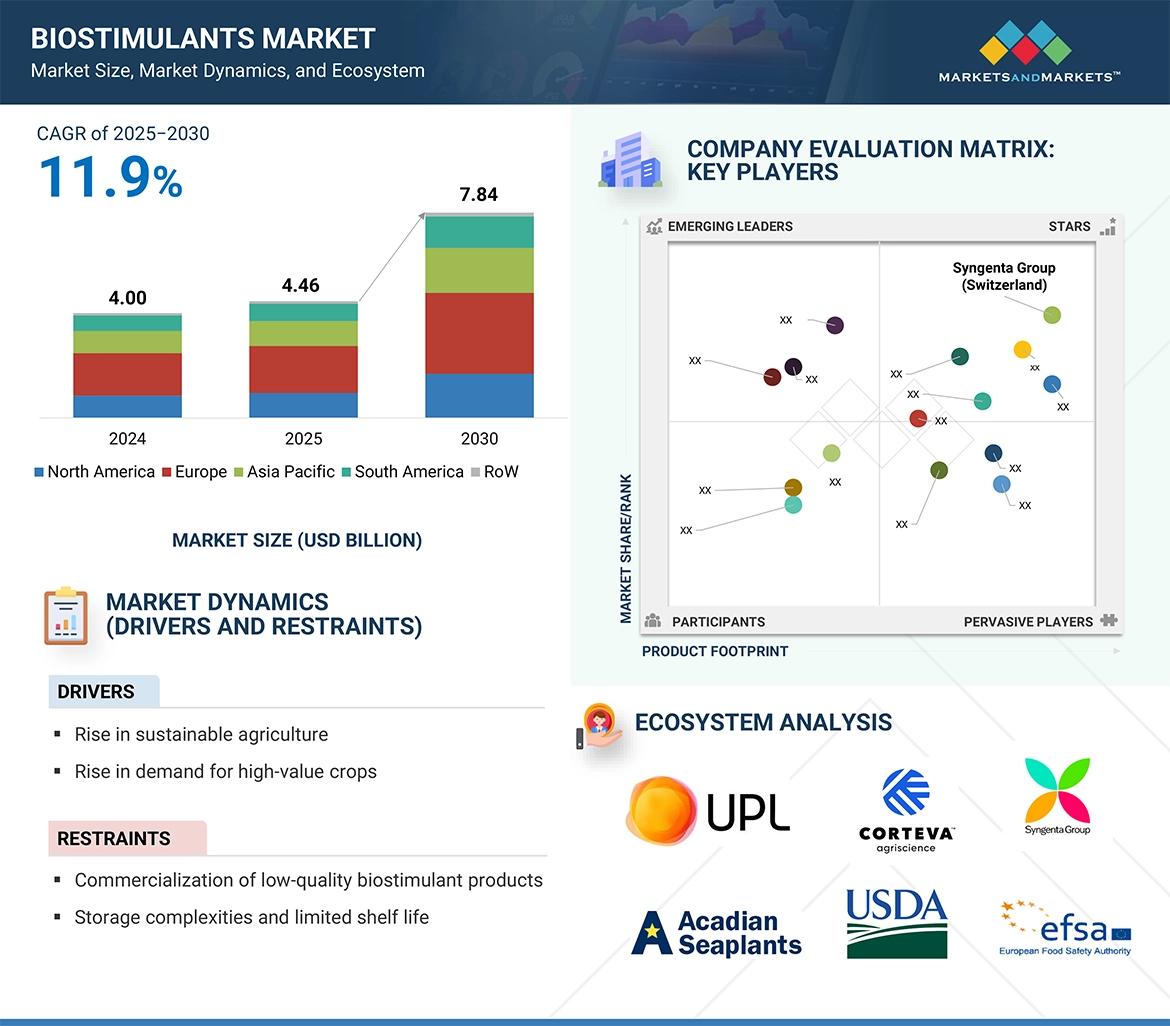

The global biostimulants market is projected to grow from USD 4.46 billion in 2025 to USD 7.84 billion by 2030, reflecting a CAGR of 11.9% during the forecast period. This robust growth is primarily fueled by the rising adoption of sustainable agricultural practices, the expanding use of organic farming, and heightened awareness about the benefits of biostimulants in enhancing crop yield, quality, and resilience to abiotic stress.

Supportive government initiatives—such as the European Union’s Farm to Fork strategy—are further accelerating market growth by promoting eco-friendly farming techniques. In parallel, advancements in biostimulant formulation and extraction technologies are improving product effectiveness and expanding their applicability across diverse crop types. Farmers are increasingly turning to biostimulants to boost nutrient efficiency, enhance soil health, and reduce dependency on chemical fertilizers. In addition, rising consumer demand for high-quality, residue-free produce is encouraging growers to incorporate biostimulants as part of their organic and sustainable farming toolkit.

By Active Ingredient: Amino Acids Lead the Market

The amino acids segment dominates the active ingredient category, owing to its critical role in supporting plant growth, enhancing nutrient uptake, and improving stress tolerance. Amino acids act as precursors to essential plant hormones, enzymes, and proteins that drive key physiological functions such as photosynthesis, nutrient assimilation, and root development. Their proven effectiveness in aiding plant recovery from abiotic stresses like drought, temperature fluctuations, and salinity makes them a preferred choice for farmers aiming to boost productivity and resilience.

One key player in this space is Aminocore (Germany), known for its natural amino acid-based fertilizers and biostimulants. Developed through mild enzymatic hydrolysis—a pharmaceutical-grade process—Aminocore’s products offer a superior free amino acid profile that is twice as effective as conventional solutions, without relying on synthetic components or toxic additives.

By Form: Liquid Biostimulants Dominate

In terms of form, the liquid biostimulants segment holds the largest market share, largely due to its ease of application, rapid absorption, and high efficacy in promoting plant growth and resistance to environmental stressors. Farmers widely favor liquid formulations as they are compatible with various application methods—including foliar sprays, fertigation, and soil drenching—ensuring uniform distribution and quick uptake by plants. Additionally, liquid biostimulants demonstrate strong compatibility with other agrochemicals and fertilizers, further enhancing nutrient absorption and crop response.

North America dominates the Biostimulants Market Share.

North America represents a substantial share of the global biostimulants market, underpinned by large-scale commercial farming, advanced agricultural technologies, and a strong focus on soil health and crop productivity. The United States and Canada lead the region with high-volume production of staple crops such as wheat, corn, and soybeans, which require consistent and efficient nutrient input.

Government support for organic and sustainable farming methods, coupled with growing awareness about the soil-enhancing and yield-boosting benefits of biostimulants, is further strengthening the market. Additionally, regional players are heavily investing in R&D to create next-generation biostimulant products with enhanced performance and wider crop applicability.

Leading Biostimulants Companies:

The report profiles key players such as UPL (India), FMC Corporation (US), Corteva (US), Syngenta Group (Switzerland), Sumitomo Chemical Co., Ltd. (Japan), Nufarm (Australia), Novonesis Group (Denmark), BASf SE (Germany), Bayer AG (Germany), PI Industries (India), T.Stanes and Company Limited (India), Gowan Company (US), J.M. Huber Corporation (US), Haifa Negev technologies LTD (Israel), and Koppert (Netherlands).