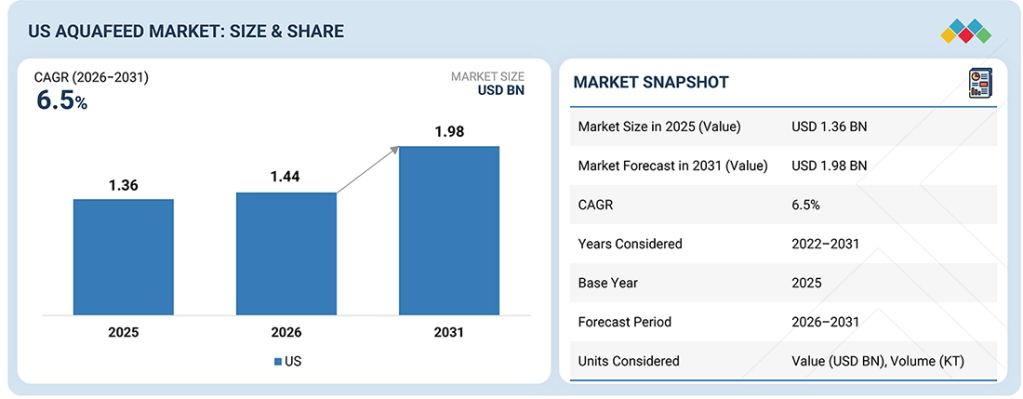

The US aquafeed market is projected to grow from USD 1.44 billion in 2026 to reach USD 1.98 billion by 2031, at a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period. The US aquafeed market is growing as demand for seafood increases and commercial fish farming grows. Farmers seek faster growth and higher survival rates for aquatic species. They prioritize efficient feed conversion and consistent production. Intensive farming systems rely on balanced formulated feed to support daily performance and minimize losses. Species like salmon, trout, catfish, and tilapia depend entirely on compound aquafeed for nutrition. Producers also emphasize feed efficiency and cost management. This fuels demand for protein-rich ingredients and functional additives. Aquaculture producers prefer diets that are scientifically validated and easy to manage. Greater focus is also placed on fish health, water quality, and sustainable farming practices. Many farms now use automated feeding systems, which facilitate the use of standard dry pellet feed. Feed directly impacts production volume, fish quality, and farm profitability. Therefore, aquafeed remains a key input in US aquaculture, maintaining steady demand across the market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=3345366

Amino acids under the additives segment of the US aquafeed market are estimated to hold the largest share in the US aquafeed market during the forecast period.

In the US aquafeed market, amino acid additives hold the largest share because they directly support faster growth, better feed efficiency, and improved protein utilization in fish and shrimp. Aquaculture producers focus on performance, uniform growth, and high survival rates. Essential amino acids such as lysine, methionine, and threonine help meet specific nutritional needs at different growth stages. They also promote muscle development and overall health. Since these benefits are clear and measurable, feed manufacturers regularly include amino acids, keeping this segment at the top.

The grower phase of the lifecycle is estimated to be the fastest-growing during the forecast period in the US aquafeed market.

The grower stage is expected to experience the fastest growth in the US aquafeed market during the forecast period. This stage lasts longer than both the hatchery and starter phases, making it essential for fish development since they gain most of their body weight during this time. To support consistent growth and ensure efficient feed conversion, farmers use large amounts of feed. As US aquaculture farms aim to boost output and shorten time-to-market, there is increased focus on the quality of grower feed. Additionally, stocking density is higher during this stage, further increasing total feed usage. Since feed costs are among the highest operating expenses for farms, producers are investing in well-balanced grower diets that promote weight gain and help protect profit margins. Due to the longer duration of this stage and the higher feed intake, the grower segment is expected to see the most significant growth in the US aquafeed market throughout the forecast period.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=3345366

Crustaceans under the species segment will register the highest CAGR during the forecast period in the US aquafeed market.

The crustacean segment in the US aquafeed market is expanding as shrimp farming increases. The USDA’s 2023 Census of Aquaculture reports 51 saltwater shrimp farms in the US, mostly in Florida and Texas, with seven inland farms in Iowa, Kentucky, Minnesota, and Missouri. Shrimp makes up about 38% of total seafood consumption in the country. The average American consumes around 5.5 pounds per year, totaling more than 1.5 billion pounds annually. However, the US imports roughly 90% of its shrimp, which opens significant opportunities for domestic production growth.

As inland and coastal shrimp farms expand, feed demand rises because shrimp rely entirely on formulated aquafeed for growth and survival. Many new farms use closed-loop Recirculating Aquaculture Systems to enhance efficiency and minimize water loss. With high consumer demand, heavy import dependence, and growing domestic production, the crustaceans’ segment is expected to grow at a faster pace in the US aquafeed market during the forecast period.

Leading US Aquafeed Companies:

The report highlights key players such as Cargill (US), ADM (US), dsm firmenich (Switzerland), Nutreco (Netherlands), Alltech (US), Purina Animal Nutrition LLC (US), Adisseo (France), Kemin Industries, Inc. (US), Darling Ingredients (US), Rangen LLC (US), The Scoular Company (US), Novus International (US), Norel Animal Nutrition (Spain), Kent Nutrition Group (US), and Beneo (Germany), among others.