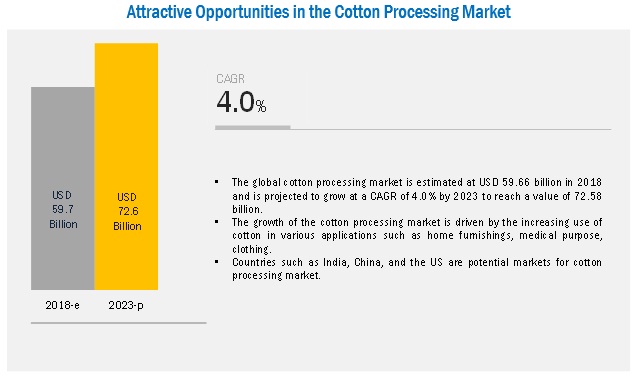

The report “Cotton Processing Market by Product (Lint, Cottonseed), Application (Textiles, Medical & surgical, Feed, Consumer goods), Equipment [Ginning (Saw, Roller), Spinning], Operation (Automatic, Semi-automatic), and Region – Global Forecast to 2023″ The market for cotton processing is estimated at USD 59.7 billion in 2018 and is projected to grow at a CAGR of 4.0% from 2018 to 2023, to reach USD 72.6 billion by 2023. The increase in demand in the textile industry, adoption of cottonseed meal as feed for ruminants, and the rising number of surgeries and operations have been propelling the consumption of cotton, leading to the rising demand for cotton processing globally.

Request for Sample Report Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=223254896

The lint segment is estimated to account for the largest share in the cotton processing market in 2018.

On the basis of product type, the cotton processing market has been segmented into lint, cottonseed, and others. The lint segment is estimated to account for the largest share in 2018. Cotton lint is widely used for manufacturing different types of surgical bandages, apparels, and household textiles. Over the years, the rise in urbanization and change in the lifestyle of consumers have led to an increase in the demand for textiles, which, in turn, is projected to drive the growth of the lint segment further.

The textile segment is estimated to dominate the cotton processing market, by application, in 2018.

The textile segment is estimated to account for the largest share of the global cotton processing market in 2018. The textile industry witnesses a significant demand for effective cotton processing techniques. Raw cotton is used as a key ingredient in the textile manufacturing applications, and there are no raw materials to substitute it. This leads to an increased demand in the textile industry. With the increasing purchasing power and technological advancements for expanding the production capacity of cotton in improving the fabric quality, the demand for processed cotton is projected to remain high globally.

The spinning segment is estimated to dominate the cotton processing equipment market, by type, in 2018.

The spinning segment is estimated to account for the largest share of the global cotton processing equipment market in 2018. Spinning is considered one of the most important processes in the textile and pharma industries and is used to convert baled cotton into yarn or thread to produce high-strength yarns. With the increasing demand for cotton in textile and medical & surgical applications, the demand for spinning is projected to remain high globally.

The automatic segment is estimated to dominate the cotton processing ginning equipment market, by type, in 2018.

The automatic segment is estimated to account for the largest share of the global cotton processing ginning equipment market in 2018. Cotton processors are increasingly focusing their attention on achieving low production costs, rapid turnaround time, and higher yields. This is facilitated by incorporating advanced automated technologies. Fully automated processing plants contribute to reduced labor costs and help in achieving operational efficiencies.

Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=223254896

Asia Pacific to be the dominant region in the cotton processing market in 2018.

Asia Pacific is estimated to be the dominant region in the cotton processing market in 2018. This is due to wide cotton cultivation in countries such as China, India, Pakistan, and Uzbekistan. The countries in the region have favorable climatic conditions for cotton production. This encourages cotton processors to invest in the cotton processing market in this region. Furthermore, growing concerns about hygiene and technological advancements in the healthcare sector in developing countries have led to an increase in the consumption of raw cotton, which, in turn, is expected to increase the demand for cotton processing solutions and equipment.

This report includes a study of marketing and development strategies along with the product portfolios of the leading companies in the cotton processing market. It includes the profiles of leading companies such as Lummus Corp (US), Bajaj Steel Industries Limited (India), Nipha Exports Private Limited (India), Shandong Swan Cotton Industrial Machinery Stock Co., Ltd. (China), Cherokee Fabrication (US), Reiter (Switzerland), and Toyota Industries (Japan).