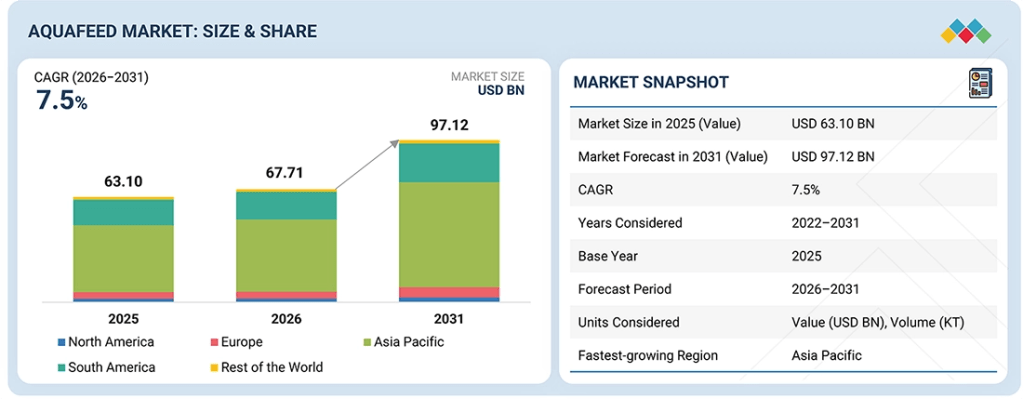

The aquafeed market is estimated at USD 67.71 billion in 2026 and is projected to reach USD 97.12 billion by 2031, at a CAGR of 7.5% from 2026 to 2031. The global population has been steadily increasing, particularly in developing countries. As more people are born and the overall population grows, food is demanded to meet their nutritional needs. With the population increase, the demand for seafood rises, leading to an increased reliance on aquaculture to meet this demand. Consequently, the demand for aquafeed, which is essential for the nutrition of farmed fish, also surges. The expanding global population creates a higher need for protein-rich food sources like seafood. With wild fisheries facing challenges such as overfishing and environmental concerns, aquaculture serves as a viable solution to meet the rising demand. However, aquaculture heavily depends on aquafeed, which traditionally includes fish meal and fish oil derived from wild-caught fish. Alternative ingredients, such as plant-based proteins and microalgae, are being explored to ensure the aquafeed market’s sustainability. This shift aims to reduce the pressure on marine resources and promote the environmentally friendly growth of aquaculture.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1151

By region, Asia Pacific to dominate market during forecast period.

Asia Pacific is estimated to be the largest market for aquafeed, and this trend is expected to persist throughout the forecast period as the sector continues to grow and develop. Key drivers include a growing emphasis on sustainability, advancements in feed formulations, and a rising demand for higher value-added, nutritionally balanced feeds.

According to the USDA’s 2024 China Fishery Products Report, China’s aquaculture sector is experiencing a notable shift toward industrialization and intensification, which is projected to boost feed demand across the region substantially. The report also states that soybean meal constitutes up to 28 percent of the feed for certain species. This heightened demand for soybean meal and other feed components directly contributes to the overall growth of the aquafeed market in the Asia Pacific region.

By additives ingredient, amino acids to hold significant market share during forecast period.

Amino acids, the fundamental building blocks of proteins, are crucial for the development of marine animals. When added to aquafeeds, they ensure that fish and other aquatic organisms receive a balanced and complete protein profile, supporting optimal growth, health, and feed conversion efficiency. Supplementing aquafeeds with essential amino acids can help producers address dietary deficiencies, improve feed utilization, and enhance the overall quality of aquaculture products.

Recent advancements in the aquafeed industry highlight a strong commitment to innovation and sustainability. A notable example is Skretting’s (India) development of the AmiNova feed formulation concept, announced in 2024. AmiNova represents a major advancement in precision nutrition for aquaculture, designed to enhance feed efficiency while reducing environmental impact. This new feed formulation is set to launch in the Chilean salmonid market in Q3 2024, with plans for expansion to other species and regions in 2025. This development solidifies amino acids’ pivotal role in advancing the efficiency and sustainability of the aquafeed market, driving continued growth and innovation in the industry.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1151

By species, crustaceans segment to register highest growth rate during forecast period.

The demand for aquafeed products has increased due to the growing prawn production for several reasons. First, high-quality, nutritionally sound feeds are required to promote shrimp growth and development as shrimp farming grows. Aquafeed supplies the necessary nutrients, vitamins, and minerals to ensure that prawns are as healthy and productive as possible. Second, as shrimp farming becomes more intensive to support greater shrimp populations, increased feed input is needed. The expanding prawn market and the need to satisfy the protein needs of a seafood-eating population are driving factors for the increased demand for aquafeed products.

Leading Aquafeed Companies:

The report profiles key players such as ADM (US), Cargill, Incorporated (US), dsm-firmenich (Switzerland), Nutreco (Netherlands), Alltech (US), Ridley Corporation Limited (Australia), Purina Animal Nutrition LLC (US), Adisseo (France), Aller Aqua Group (Denmark), Avanti Feeds Limited (India), The Waterbase Limited (India), JAPFA Ltd. (Singapore), Charoen Pokphand Foods PCL (Thailand), BioMar Group (Denmark), Norel Animal Nutrition (Spain), and others.