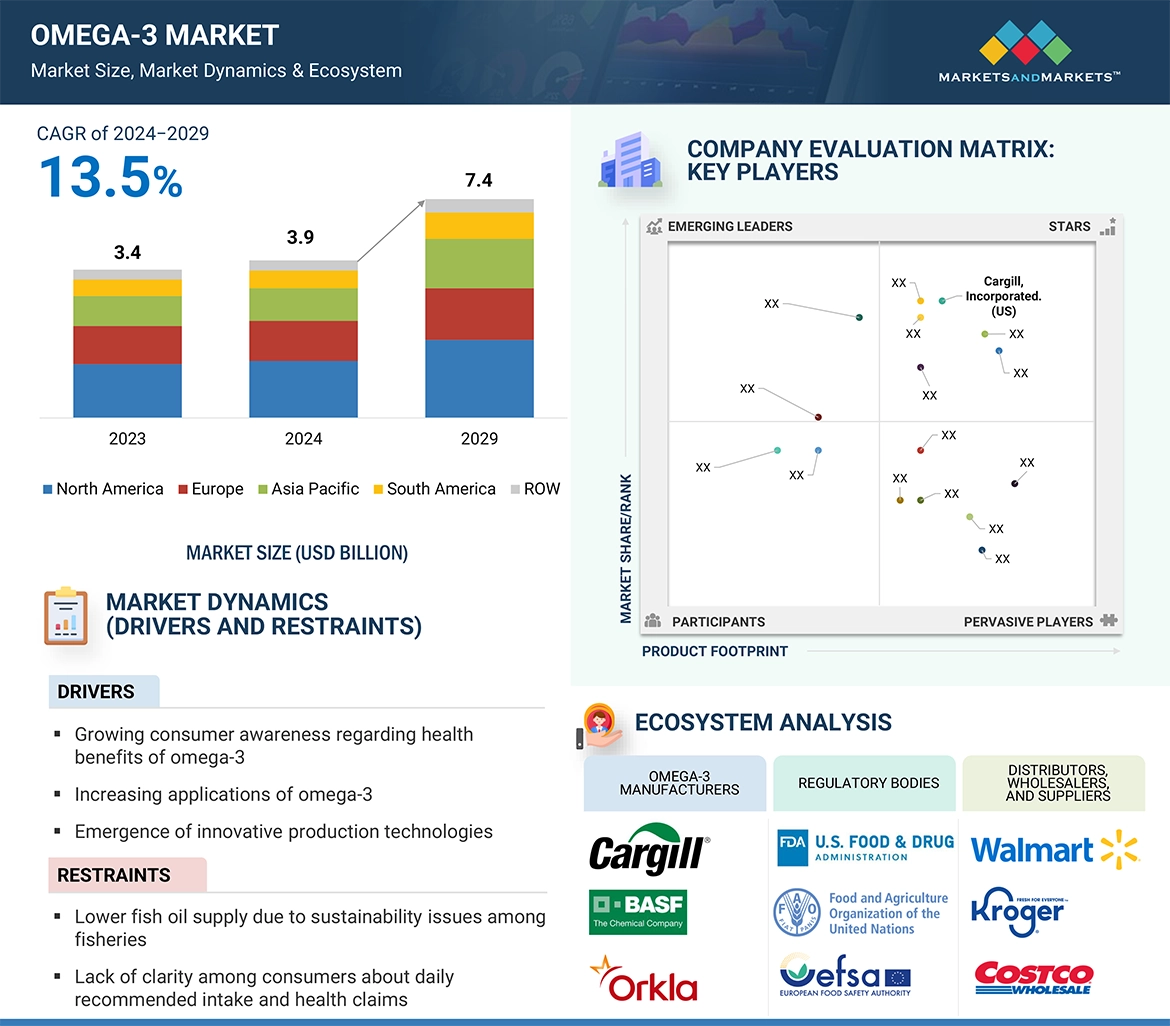

The global omega-3 market is expected to grow from USD 3.9 billion in 2024 to USD 7.4 billion by 2029, registering a robust CAGR of 13.5% during the forecast period. This impressive growth is driven by a shift in consumer preferences towards proactive health management, ethical consumption, and functional nutrition.

Evolving Sources: Beyond Traditional Fish Oil

While fish oil has long dominated the omega-3 market, sustainable and plant-based alternatives such as algae, flaxseed, and chia seed oils are gaining traction. These options appeal to health-conscious consumers with dietary restrictions, ethical concerns, or environmental awareness. In addition, emerging product formats—like micro-emulsified supplements and omega-3-fortified foods—are making consumption more convenient and appealing across broader age and lifestyle demographics.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=227

DHA Leads the Way in Omega-3 Types

Among the omega-3 types, docosahexaenoic acid (DHA) is expected to hold the largest market share. Widely recognized for its vital role in brain development, heart health, and vision support, DHA is increasingly incorporated into targeted applications such as prenatal supplements, infant formula, and functional foods. Technological advancements have improved extraction and processing methods, making DHA more accessible and versatile. Although DHA dominates, other omega-3 forms like EPA and ALA are also witnessing steady growth, contributing to a diverse and inclusive market.

Plant-Based Omega-3s: A Green Growth Trajectory

The plant-sourced omega-3 segment is set to maintain strong growth, powered by rising demand for vegan, vegetarian, and allergen-free alternatives. Algae-derived omega-3s and chia seed extracts are especially popular for their sustainability and potential health benefits. Supportive government policies promoting eco-friendly practices and the growing affordability of these alternatives further reinforce their market potential. Overcoming challenges such as bioavailability and consumer education will be crucial in unlocking the segment’s full potential.

North America: A Leading Market for Omega-3

North America currently holds the largest share of the omega-3 market, driven by widespread adoption of dietary supplements and increased awareness of omega-3’s health benefits. With strong consumer interest in heart, brain, and overall wellness, omega-3 supplements have become a staple in health routines across the region. In addition, incorporation of omega-3 in medical guidelines and wellness trends is fueling sustained demand.

Leading Omega-3 Companies:

BASF SE (Germany), Cargill, Incorporated (US), dsm-firmenich (Netherlands), ADM (US), Kerry Group Plc (Ireland), Croda International Plc (UK), Orkla (Norway), Corbion (Netherlands), Pelagia AS (US), KD Pharma Group SA (Switzerland), GC Rieber (Norway), Cooke Aquaculture (Canada), AlgiSys Biosciences, Inc. (US), Golden Omega (Chile), AKER BIOMARINE (Norway), Polaris (France), Nordic Naturals (US), BTSA (Spain), Farbest Brands (US), KinOmega Biopharm Inc (China), Pharma Marine AS (Norway), Rimfrost AS (Norway), Algarithm (Canada), Solutex (Spain), Cellana Inc (US), Sinomega Biotech Engineering Co., Ltd. (China), AlgaeCytes (UK).