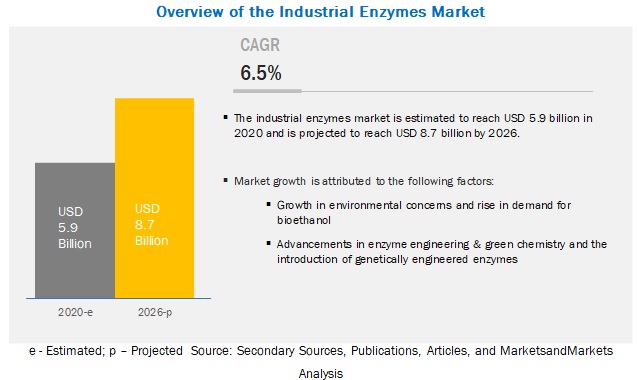

The report “Industrial Enzymes Market by Type (Carbohydrases, Proteases, Lipases, Polymerases & Nucleases, Other Types), Source, Application (Food & Beverages, Feed, Bioethanol, Detergents, Pulp & Paper, Textiles & Leather, Wastewater Treatment, Other Applications), Form, and Region – Global Forecast to 2026″ According to MarketsandMarkets, the industrial enzymes market is estimated to be valued at USD 5.9 billion in 2020 and is projected to reach USD 8.7 billion by 2026, recording a CAGR of 6.5%, in terms of value. The growing environmental concerns and enzyme quality in food & beverages and feed, and the rising demand for bioethanol are factors that are projected to drive the growth of the industrial enzymes market globally.

The microorganism segment is projected to witness significant growth during the forecast period.

Based on source, the industrial enzymes market is segmented into microorganism, plant, and animal. The microorganism segment is projected to witness the fastest growth during the forecast period, as enzymes obtained from microbial sources lead to low production costs. Furthermore, they contain more predictable and controllable enzyme content. In addition, as enzymes obtained from microbial sources can be cultured in large quantities in a short period, microorganisms are the primary source of industrial enzymes.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=237327836

The carbohydrases segment is projected to account for a major share in the industrial enzymes market during the forecast period

By type, the industrial enzymes market is segmented into carbohydrases, proteases, lipases, polymerases & nucleases, and other enzymes (such as catalases, laccases, oxidases, phosphatases, kinases, esterases, and pectinases). Carbohydrases are classified into amylases, cellulases, and other carbohydrases (such as pectinases, lactases, mannanases, and pullulanases). Amylases used in the textile industry benefit denim manufacturers in de-sizing and lowering the operational costs. In the paper industry, amylases help in de-inking and drainage improvement. However, the textile industry functionally benefits in the replacement of pumice stones by a cellulose-based treatment; benefits include less damage to fibers, increased productivity of the machines, and less hazardous environment for manufacturers.

The North American region dominated the industrial enzymes market with the largest share in 2019, whereas Asia Pacific is expected to witness the highest growth rate.

The industrial enzymes market in North America was dominant due to the increasing demand for enzymes in industrial applications. Technological innovations in machinery, optimization of production, logistics, and globalization of business have made the food & beverage industry one of the essential sectors in North America. However, the shift of industrial operations from developed regions, such as North America and Europe, to Asia Pacific, has further contributed to the growth of the industrial enzymes market in the Asia Pacific region. The use of industrial enzymes in textiles & leather and detergents has been fueling the market in the Asia Pacific region. Furthermore, European consumers have shown an inclination toward clean-label and organic products. This has enabled manufacturers to consider organic ingredients as major components of the products. Due to this, the industrial enzymes market in the European region is led by the growing focus on the production of food & beverages, owing to the functional benefits of enzymes.

This report includes a study on the marketing and development strategies, along with the product portfolios of leading companies. It consists of profiles of leading companies, such as BASF (Germany), Novozymes (Denmark), DuPont (US), DSM (Netherlands), Kerry Group (Ireland), Dyadic International (US), Advanced Enzymes (India), Chr. Hansen (Denmark), Amano Enzymes (Japan), Megazyme (Ireland), Aumgene Biosciences (India), Biocatalysts (UK), Enzyme Supplies (UK), Creative Enzymes (US), Enzyme Solutions (US), Enzymatic Deinking Technologies (US), Sunson Industry Group (China), MetGen (Finland), Denykem (UK), and Tex Biosciences (India).