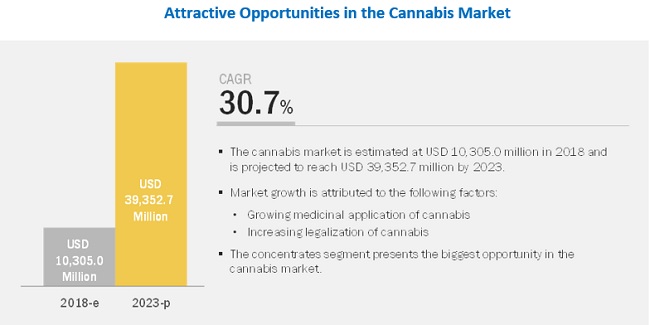

The global cannabis market size is projected to grow from USD 10.3 billion in 2018 to USD 39.4 billion by 2023, at a Compound Annual Growth Rate (CAGR) of 30.7% during the forecast period. The major driving factors in the cannabis market are growing medicinal application of cannabis and increasing legalization of cannabis.

The global market for cannabis is dominated by major players such as Canopy Growth Corporation (Canada), Aurora Cannabis Inc. (Canada), Tikun Olam (Israel), Cannabis Science Inc. (US), Aphria Inc. (Canada), Maricann Group Inc. (Canada), Tilray Inc. (Canada), VIVO Cannabis Inc. (Canada), Medical Marijuana, Inc. (US), STENOCARE (Denmark), Cronos Group Inc. (Canada), Terra Tech Corp. (US), and MedMen (US). These players have adopted various growth strategies such as agreements, collaborations, joint ventures & partnerships, new product launches, expansions & investments, and acquisitions to expand their presence in the global cannabis market. Agreements, collaborations, joint ventures & partnerships have been the most dominating strategies adopted by the major players from 2013 to 2018. These strategies have helped them to tap the lucrative growth opportunities in the market and strengthen their market positions. Additionally, they have also helped them to increase their distribution channels.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=201768301

Canopy Growth Corporation has been focusing on mergers & acquisitions and various agreements to expand its reach across different provinces of Canada as well as other countries such as Australia, Chile, Denmark, Lesotho, and Spain. The company is also strategizing to focus on upcoming products in the cannabis industry. For instance, in October 2018, the company acquired Eddu (Colorado) for the manufacturing of innovative products, such as cannabis-infused beverages. Moreover, Constellation Brands (US) has invested USD 4 billion in Canopy Growth Corporation to the company to strengthen its position and establish widespread operations across 30 countries.

Aurora Cannabis Inc. acquired and partnered with many companies to build a strong presence in terms of geographic reach, technology, production, and product offering. It is the only company that has launched a mobile application for ordering medically prescribed cannabis that will help the patients to order in a more user-friendly way. Additionally, to target the emerging consumption of cannabis among adults, it has been associating with liquor manufacturers to resell their recreational cannabis product. In September 2018, Aurora Cannabis Inc. acquired Agropro UAB (Lithuania) and Borela UAB (Lithuania) to extract and produce CBD-based wellness products for the European market.