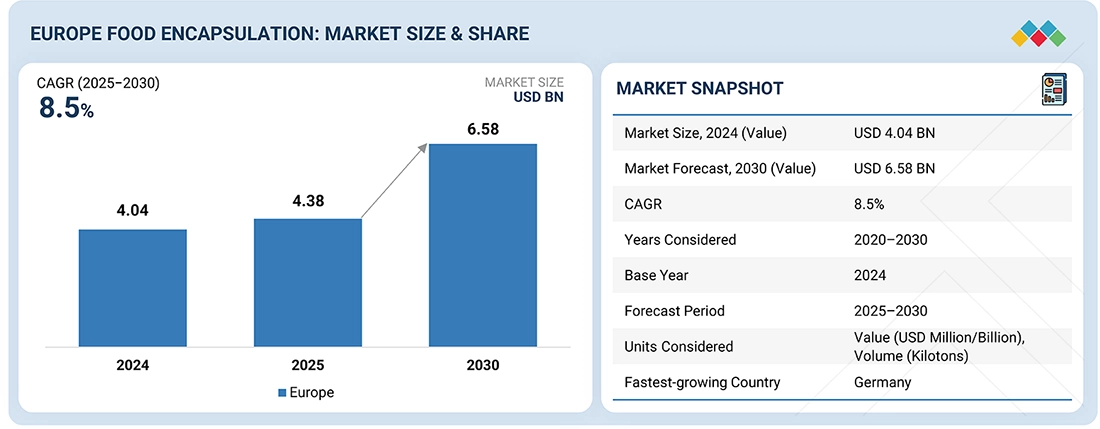

The North America food encapsulation market is valued at USD 4.68 billion in 2025 and is projected to reach USD 6.98 billion by 2030, expanding at a compound annual growth rate (CAGR) of 8.3% over the forecast period. The market is experiencing steady growth as food manufacturers increasingly adopt encapsulation technologies to protect sensitive ingredients such as vitamins, minerals, probiotics, enzymes, flavors, and omega-3 oils from exposure to heat, moisture, and oxygen. Encapsulation improves ingredient stability throughout processing and storage, ensuring functional performance and product quality across the supply chain.

The rising demand for functional and fortified foods is a major growth driver. Encapsulation is widely used in dairy products, bakery items, beverages, and nutrition products to manage ingredient behavior, enable controlled release, improve absorption, and mask strong or unpleasant tastes. Established large-scale production methods such as spray drying, extrusion, and emulsion technologies continue to dominate due to their efficiency, scalability, and industrial reliability.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=114459686

Functional Foods Lead Market Applications

By application, functional food products account for the largest share of the North America food encapsulation market. Encapsulation enables the integration of active ingredients into everyday foods without compromising stability, taste, or shelf life. Consumer demand for foods that support health, immunity, digestion, and energy is driving the growth of fortified dairy, cereals, bakery products, and nutrition bars. Food manufacturers increasingly rely on encapsulation to meet both performance standards and clean-label expectations, reinforcing this segment’s dominant position in the market.

Nanoencapsulation Emerges as the Fastest-Growing Technology

By technology, nanoencapsulation is projected to be the fastest-growing segment in the market. Nano-scale delivery systems enable enhanced protection of bioactive compounds, improved ingredient dispersion, and precise control over release mechanisms during digestion. These capabilities support the growing use of bioactive ingredients in functional and fortified foods. As manufacturers move toward high-performance, precision-driven formulations, nanoencapsulation adoption is accelerating faster than traditional encapsulation technologies.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=114459686

United States Drives Regional Growth

On a country basis, the United States is recording significant growth within the North America food encapsulation market. Strong adoption across food and beverage manufacturers, advanced processing infrastructure, and robust R&D ecosystems are supporting rapid commercialization of encapsulated ingredients. Encapsulation is widely used to enhance ingredient stability, extend shelf life, and improve sensory performance in packaged foods. Expansion of health-focused product lines across supermarkets, mass retailers, and e-commerce platforms, combined with clear regulatory standards, continues to reinforce the U.S. as a key growth engine for the regional market.

The report profiles key players such as Cargill, Incorporated (US), Ingredion (US), Sensient Technologies Corporation (US), Balchem Corporation (US), Encapsys LLC (US), International Flavors & Fragrances Inc. (US), DuPont (US), Aveka Group (US), Microtek Laboratories, Inc. (US), and Innophos Holdings, Inc. (US).