The ongoing COVID-19 pandemic—and the worldwide reaction to it—has compelled companies to radically rethink their strategies and the way they operate. We salute the industry experts helping companies survive and sustain in this pandemic.

At MarketsandMarkets™, analysts are undertaking continuous efforts to provide analysis of the COVID-19 impact on the Lutein Market. We are working diligently to help companies take rapid decisions by studying:

- The impact of COVID-19 on the Lutein Market, including growth/decline in product type/use cases due to the cascaded impact of COVID-19 on the extended ecosystem of the market

- The rapid shifts in the strategies of the Top 50 companies in the Lutein Market

- The shifting short-term priorities of the top 50 companies’ clients and their client’s clients

You can request an in-depth analysis detailing the impact of COVID-19 on the Lutein Market: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=69753879

Lutein is an important carotenoid antioxidant that is used for protecting eye health. It is also used in animal feed to color the poultry skin and egg yolks to strengthen the immune system, reduce cellular aging, and protect against age-related eye diseases.The overall growth of the lutein market is driven by the rise in demand for its usage as an eye health supplement andits increased usage as an animal feed additive and as a natural colorant; and its usage in other healthcare and nutraceuticals applications.

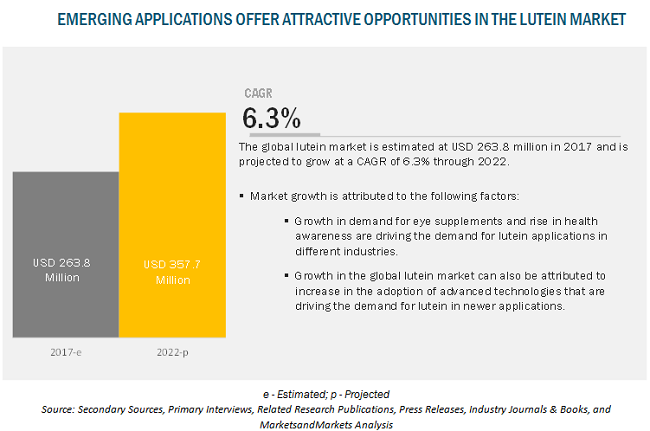

The global market for lutein is projected to reach USD 357.7million by 2022, recording a CAGR of 6.3%

On the basis ofform, the powder & crystallinesegment is projected to dominate the lutein market. Lutein is mainly used in the powdered form, as it is easy to use and can be added to various solutions and liquids in the livestock feed, food, and cosmetics industries. Furthermore, the powder & crystalline form of lutein reduces eye fatigue and glare sensitivity; strengthens eye tissue; supports brainfunction and enhances memory; maintains heart health; and protects skin health.

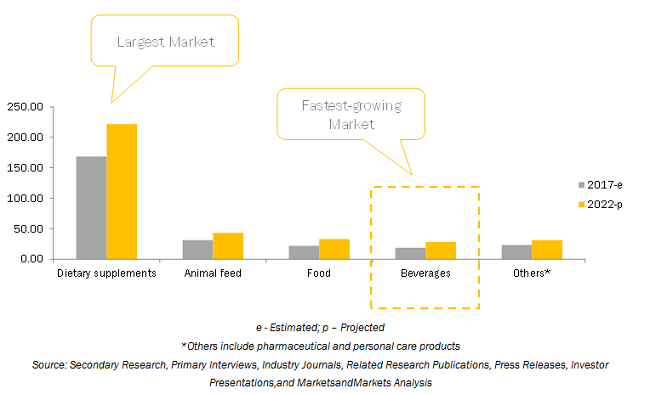

Dietary supplements – the most promising market for lutein in the next five years

With the aging population, people are becoming more conscious and aware of age-related problems. Cataracts and age-related macular degeneration (AMD) are the major illnesses faced by aged people, which cause visual impairment and acquired blindness. This is due to the lack of intake of sufficient nutrients, such as green leafy vegetables and egg yolks. This concern has boosted the demand for health supplements, thus fueling the growth of the lutein market.

Furthermore, consumers have become aware of the alternative channels to self-diagnose themselves and also take preventive measures to remain healthy. Such practices are significantly increasing the demand for supplements, globally, which, in turn, drives the consumption of lutein.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=69753879

Geographical Prominence

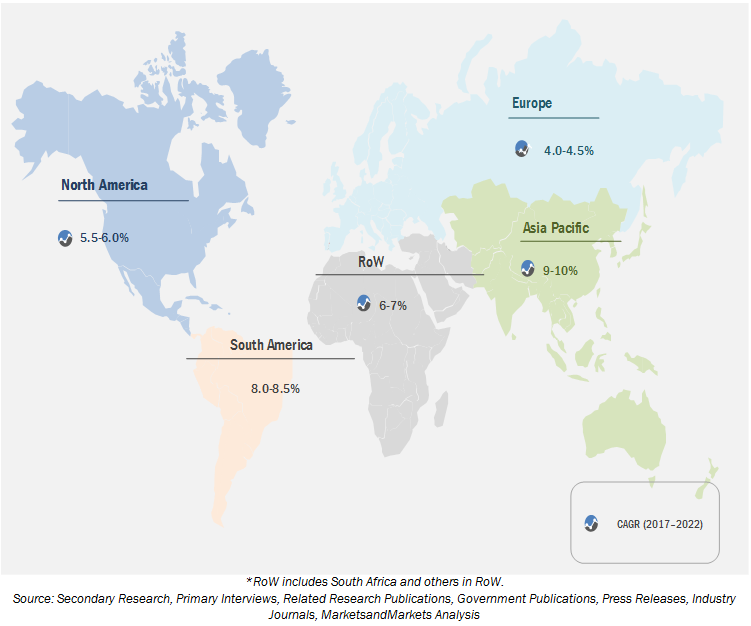

The European region is estimated to account for the largest market share in the global lutein market. This market is also projected to grow at a CAGR of 4.3 % from 2017 to 2022 to reach USD 130.2 million by 2022 moderately. The market for Asia Pacific is expected to register the highest growth during the forecast period, owing to the increase in health awareness and rise in penetration of functional food and dietary supplements. Furthermore, the market is growing due to the rising demand for eye supplements in the healthcare sector. The rise in the prevalence of diseases such as heart diseases, diabetes, obesity, and stroke are also expected to drive the demand for lutein dietary supplements, which include minerals, fatty acids, and vitamins.

Conclusion

Globally, lutein finds application in various industries due to its nutritional benefits and pigmentation properties. Lutein is extensively used as an additive to provide food colors, either by directly applying them to food products or indirectly adding them to animal feed. Due to its medicinal properties, lutein is widely used in pharmaceuticals for preventive medicines in eye care, cardiac diseases, diabetes, and skincare. It is currently extensively used in health supplements due to the rising demand for the same by health-conscious customers.

Considering the importance of supplementation, globally, major companies are increasingly inclined to invest in scientific research to develop new applications for lutein that can help improve human health. Key players in this market have adopted various strategies such as expansions, acquisitions, new product launches, among others,to expand their global footprint and increase their product offerings to capture the market share. The lutein market is competitive, with many large players such as BASF (Germany), Chr. Hansen (Denmark), E.I.D. Parry (India), Kemin (US), Zhejiang Medicine (China), and OmniActive (India) who focus on expanding their market base in this field.