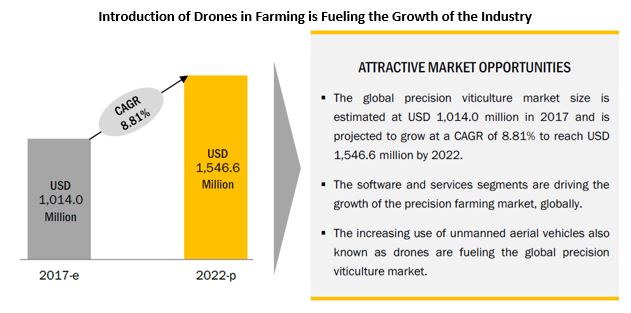

The global precision viticulture market is estimated to be valued at USD 1,014.0 Million in 2017 and is projected to grow at a CAGR of 8.81% from 2017 to 2022. The key players in the precision viticulture market include John Deere (US), Trimble (US), Topcon (Japan), Deveron UAS (Canada), and TeeJet Technologies (US). Other players in the precision viticulture market include Groupe ICV (France), Tracmap (New Zealand), QuantisLabs (Hungary), Terranis (France), Ateknea Solutions (Spain), AHA Viticulture (Australia), and AG Leader Technology (US).

Strategic acquisitions and organic expansions were the core strengths of the leading players in the precision viticulture market; these strategies were adopted by the players to increase their market presence. They also helped the players diversify their businesses geographically, strengthen distribution networks, and enhance their production capacities. Market leaders such as Deere & Company (US), Trimble (US), and Topcon (Japan), successfully tapped the potential markets through expansions, investments, acquisitions, agreements, and joint ventures.

John Deere (US) is one of the leading companies in the precision viticulture industry. The company develops displays & receivers to be used for the tracking of vineyards in precision viticulture. The field and crop solutions manufactured by the company can be used with smart devices which can be remotely operated using local or cloud connectivity. The company mainly focuses on strategies such as partnerships and acquisitions in order to increase its footprint globally. For instance, in 2017, John Deere acquired ag-tech startup, Blue River Technology (US), in order to expand its integrated computer vision and machine learning technology product portfolio. Strong global presence and well-established R&D activities are the major factors contributing to the high potential of this company in the precision viticulture market.

Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=116965282

Trimble (US) is a leading company in the precision viticulture market; it is a manufacturer of hardware & software and a service provider of a broad range of precision viticulture solutions for vineyards and vine growers. Trimble works in close cooperation with its growers and farmers to meet the requirements of precision viticulture to minimize water consumption and weed development in vineyards. The company aims to increase its business in emerging as well as established markets to develop a significant global reach by adopting organic and inorganic strategies. For instance, between 2016 and 2018, the company launched five new products including IoT sensor, agriculture software, and GNSS boards catering to the increasing demand from vine growers.

The Asia Pacific region is projected to grow at the highest CAGR from 2017 to 2022.

The Asia Pacific region is projected to grow at the highest CAGR during the forecast period. The countries covered under the region include Australia & New Zealand, China, India, Japan, and the Rest of Asia Pacific which includes Thailand, Vietnam, Indonesia, Malaysia, the Philippines, and South Korea. Increasing awareness about the implementation of innovative technologies for valuing spatial data and mapping yields of grapes in emerging economies such as Australia & New Zealand and India are the key factors that drive the precision viticulture market growth in the region. The presence of large farmlands and increasing adoption of agricultural technologies in the countries drive the demand for precision viticulture in the region.