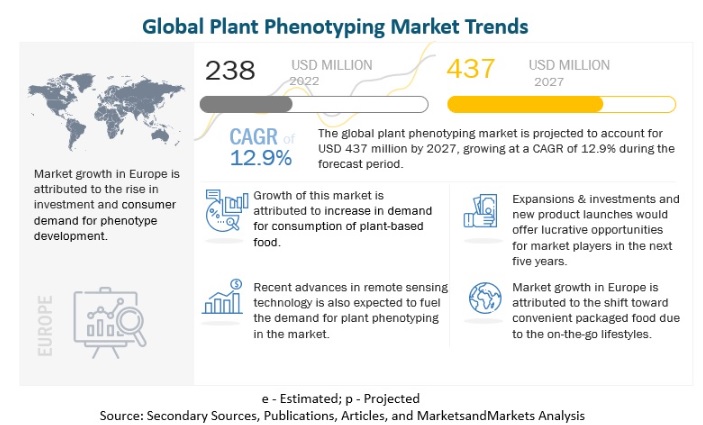

The global plant phenotyping market is on a significant growth trajectory, with an anticipated value of USD 437 million by 2027, fueled by a robust compound annual growth rate (CAGR) of 12.9% during the forecast period. The market is witnessing increased expansions and investments in plant phenotyping in developed regions, serving as a primary driver for its rapid growth. Furthermore, the growing emphasis on sustainable crop production through improved crop varieties is a pivotal factor bolstering the market for plant phenotyping.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=236591018

In developed regions, a substantial focus on funding for plant phenotyping experiments by governments and various organizations, particularly in Europe and North America, has played a crucial role in the expansion of the plant phenotyping market. These investments are aimed at advancing agricultural practices and ensuring sustainable crop production to meet the food, fuel, and feed demand for their growing populations while adapting to changing climatic conditions.

The Asia Pacific region, including developing countries, is emerging as a hotspot for the demand of plant phenotyping products and services. These nations are grappling with the challenge of ensuring food security and sustainable agriculture for their expanding populations. Additionally, they are seeking to develop crops that can thrive in the face of shifting climatic conditions, further driving the adoption of plant phenotyping technologies.

Key players in the plant phenotyping market include renowned plant phenotyping product manufacturers like LemnaTec GmbH (Germany), Delta-T Devices Ltd. (UK), CropDesign – BASF SE (Germany), Heinz Walz GmbH (Germany), Phenospex B.V. (Netherlands), WPS (Netherlands), Phenomix (France), Photon Systems Instruments (Czech Republic), and Qubit Systems (Qubit Phenomics) (Canada). The market also features service providers, such as KeyGene N.V. (Netherlands), Rothamsted Research Limited (UK), The Vienna Biocenter Core Facilities GmbH (VBCF) (Austria), and Equinom (Netherlands). These companies are at the forefront of innovation, continually enhancing their products and services based on advanced spectrometry and imagery techniques.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=236591018

In 2022, the image analysis segment is projected to dominate the plant phenotyping market, representing the largest share. Image analysis tools serve as standalone or additional accessories that can be integrated into plant phenotyping equipment systems. While equipment systems typically include default software, the increasing demand for diverse applications has driven the integration of additional software and sensors, allowing customization according to the specific needs of end-users, including service providers and research organizations.