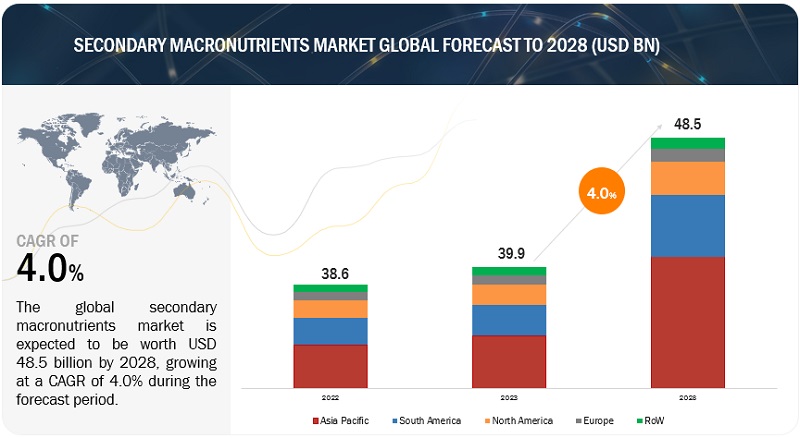

In the dynamic landscape of global agriculture, the secondary macronutrients market has emerged as a pivotal player, with an estimated value of USD 38.6 billion in 2022 and a projected ascent to USD 48.5 billion by 2028. This promising growth trajectory, at a Compound Annual Growth Rate (CAGR) of 4.0% from 2023 to 2028, is attributed to the escalating demand for essential foods like cereals, grains, fruits, and vegetables.

Farmers, attuned to the invaluable role of secondary macronutrients in enhancing crop production, are increasingly turning to these fertilizers to amplify yields and improve overall crop quality. This trend is a key driver propelling the market forward.

View detailed Table of Content here: https://www.marketsandmarkets.com/Market-Reports/secondary-macronutrient-market-45874881.html

South America emerges as the torchbearer of growth in the secondary macronutrients market, boasting the title of the fastest-growing region. With a robust agricultural sector contributing significantly to the regional economy, the adoption of secondary macronutrient fertilizers proves instrumental for farmers seeking to augment crop yields and profitability. The increasing availability and cost-effectiveness of these fertilizers further catalyze their utilization, with South American nations exporting agricultural products to meet stringent quality standards in global markets.

Key players in the secondary macronutrients market, including Nutrien Ltd., Yara, The Mosaic Company, and others, play a pivotal role in shaping the industry landscape. Their contributions underscore the importance of strategic initiatives and innovations in driving market growth.

Fruits and vegetables emerge as the fastest-growing segment during the forecast period. The surge in veganism and vegetarianism fuels heightened demand for plant-based foods, necessitating increased cultivation of fruits and vegetables. A growing awareness of the health benefits associated with consuming these plant-based foods further propels the demand for secondary macronutrients in agriculture.

The versatility of delivering secondary macronutrients in liquid form proves to be a game-changer for farmers. Through foliar sprays, fertigation, and soil drenches, farmers can tailor their approach to suit the specific needs of their crops and growing environments. The simplicity of combining liquid forms with water or other fertilizers ensures a homogeneous solution, promoting uniform nutrient dispersion across fields. This strategic approach results in more consistent crop development and, ultimately, higher yields.

To Know More Get PDF Copy: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=45874881

In conclusion, the secondary macronutrients market stands at the forefront of agricultural innovation, driven by a confluence of factors such as rising food demand, heightened agricultural awareness, and the strategic adoption of advanced delivery methods. As the global agricultural landscape continues to evolve, the role of secondary macronutrients in optimizing crop production is set to become increasingly pronounced, heralding a new era of sustainable and high-yield agriculture.