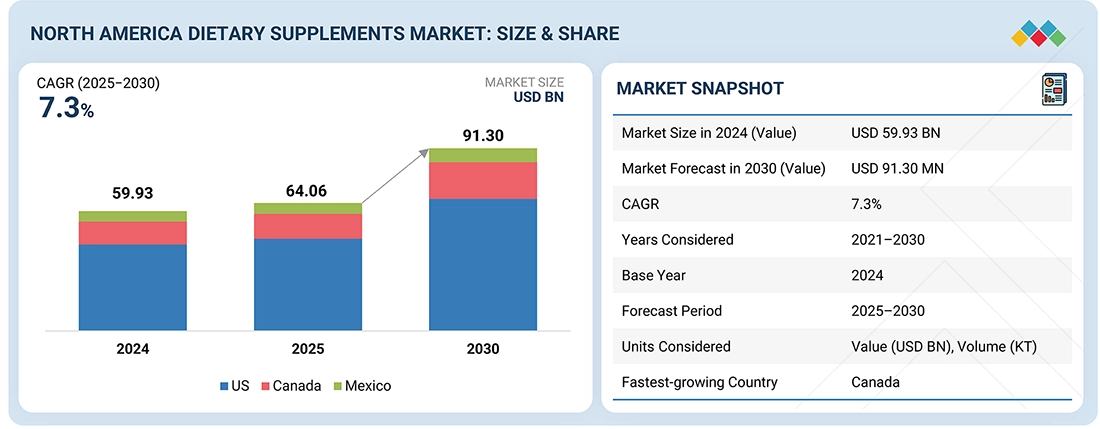

According to MarketsandMarkets™, The North America dietary supplements market is poised for strong growth, projected to expand from USD 64.06 billion in 2025 to USD 91.30 billion by 2030, registering a compound annual growth rate (CAGR) of 7.3% during the forecast period. Market expansion is primarily fueled by the rising adoption of preventive health and wellness practices, growing demand for plant-based and clean-label supplements, and the continued rise of sports nutrition and lifestyle fitness trends.

The market is expected to grow at a rapid pace as consumers increasingly seek proactive solutions to manage their health. Advancements in supplement delivery formats—such as gummies, effervescent tablets, and personalized nutrition solutions—along with the rising healthcare burden caused by chronic diseases, are further accelerating demand across the region.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=204852544

Vitamins Segment Leads by Type

By type, the vitamins segment is anticipated to dominate the North America dietary supplements market. Vitamins remain the most widely recognized and trusted supplement category, strongly associated with immunity, energy, and overall wellness. Their broad acceptance and integration into daily preventive health routines continue to make them the preferred choice among consumers.

Gut Health, Immune Health, and Sports Nutrition Drive Functional Demand

Based on function, gut health, immune health, and sports nutrition represent the key growth areas in the market. A healthy gut plays a vital role in enhancing nutrient absorption, supporting immune responses, and aiding the synthesis of essential vitamins and neurotransmitters, making gut health supplements increasingly important for holistic well-being.

Adults Remain the Largest Target Consumer Group

By target consumer, the adult segment accounts for a significant share of the market, driven by a growing focus on preventing chronic conditions such as heart disease, diabetes, and joint-related disorders. This trend is boosting demand for multivitamins, minerals, and specialty supplements tailored to adult health needs.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=204852544

Canada Emerges as the Fastest-Growing Market

Among North American countries, Canada is expected to register the highest CAGR during the forecast period. Growth in the Canadian dietary supplements market is supported by an aging population, increasing health awareness, and a rising inclination toward self-care and preventive healthcare solutions.

Leading North America Dietary Supplements Companies:

Major companies operating in the North America dietary supplements market include Nestlé (Switzerland), Abbott (US), Haleon Group of Companies (UK), Otsuka Holdings Co., Ltd. (Japan), Glanbia plc (Ireland), Bayer AG (Germany), H&H Group (Hong Kong), Amway Corp (US), American Health (US), Nature’s Sunshine Products, Inc. (US), and Herbalife International of America, Inc. (US).

These players continue to focus on product innovation, clean-label formulations, and strategic expansions to strengthen their presence in the rapidly evolving dietary supplements landscape.