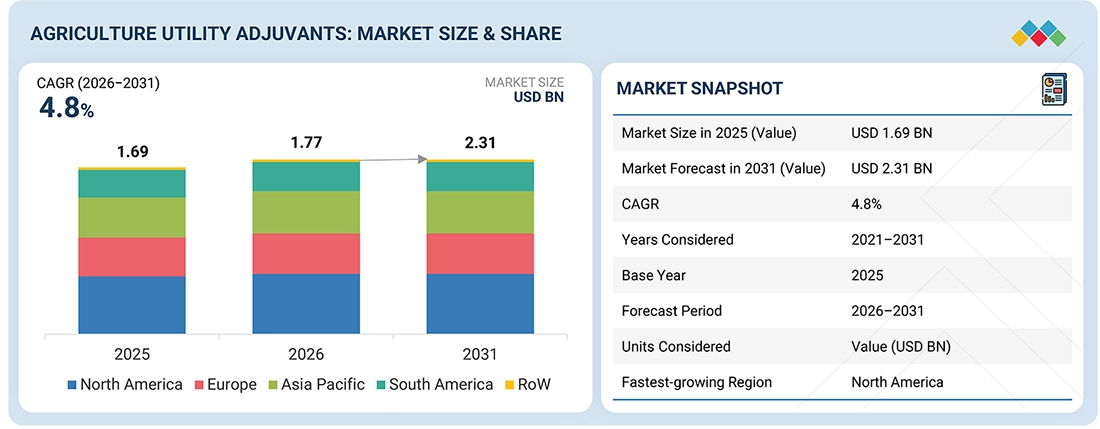

The agriculture utility adjuvants market is projected to reach USD 2.31 billion by 2031 from USD 1.77 billion in 2026, at a CAGR of 4.8% from 2026 to 2031. The global utility adjuvants market is experiencing rising demand due to increased attention from farmers on optimizing the quality of spray water, tank mixes, and the effectiveness of crop protection agents. Stricter government regulations concerning environmental safety, spray precision, and pesticide use have further supported market growth. The adoption of precision farming techniques has also created a need for more reliable spray solutions. Additionally, manufacturers are increasingly emphasizing the use of water conditioners, buffering agents, anti-foaming agents, and compatibility enhancers to improve the physical and chemical stability of spray mixtures. Utility adjuvants play a vital role in neutralizing hard water minerals, maintaining pH levels, controlling foam formation, and ensuring the compatibility of multiple agrochemicals in the same spray tank. Rising farmer interest in effective application methods and reducing chemical wastage is also driving the development of advanced utility adjuvants to boost operational efficiency and preserve active ingredients. As modern agriculture continues to evolve toward higher productivity and sustainability through precision practices, the utility adjuvants market is expected to remain a key part of the global crop protection industry.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=131568926

The emulsifiable concentrates segment holds a significant market share in the formulation segment.

Emulsifiable concentrates (EC) also hold a significant market share in the formulation segment of the utility adjuvants market because of their excellent compatibility and ability to blend with crop protection products. This formulation type allows for the emulsification of oil-soluble functional ingredients to mix with water in the spray tank, ensuring an even distribution of active and performance-enhancing ingredients. The capacity to maintain solution stability across varying water qualities and conditions makes this formulation type suitable for large-scale agricultural spraying activities.

Furthermore, using emulsifiable concentrates improves the functional efficiency of utility modifiers, which in turn enhances mix qualities, prevents separation, and makes product application easier through spraying. Additionally, the product’s versatility, including herbicides, fungicides, and insecticides, boosts its market viability. Moreover, the growing demand for versatile, ready-to-mix liquid formulations that work in diverse climates increases the dominance of the emulsifiable concentrates segment in the formulation market.

In the application segment, herbicides is the fastest-growing segment in the global agricultural adjuvants market.

The global agricultural utility adjuvants market is growing fastest in the herbicide application segment. The increased adoption of herbicides to combat rising weed resistance issues, along with the expanding use of conservation tillage methods, drives this growth. Spraying adjuvants improve herbicide effectiveness by enhancing spray coverage, droplet retention, cuticle penetration, and rainfastness, leading to better active ingredient performance. The agriculture industry needs utility adjuvants to meet the growing demand driven by precision spraying technology and tank-mix applications for herbicides. Dual pressures from regulations demanding better pesticide practices and environmental protection motivate farmers to use adjuvants for effective weed control at lower chemical application levels.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=131568926

Based on region, Europe holds a significant share in the global agricultural utility adjuvants market.

Based on the region-wise segmentation, Europe has emerged as a prominent player in the global utility adjuvants market due to its strong regulatory environment and focus on sustainable agriculture. The region has implemented strict policies regarding pesticide use, drift prevention, water conservation, and environmental safety. These regulations have increased the demand for high-quality water conditioners, buffering agents, compatibility agents, and anti-foaming agents to ensure the responsible use of agrochemicals. Additionally, the adoption of precision agriculture tools, such as variable-rate sprayers and digital spray-monitoring devices, is very high in Europe. These tools require well-conditioned and stable spray solutions to perform optimally, which also drives demand for utility adjuvants. Furthermore, Europe’s well-established agrochemical industry, ongoing R&D efforts in formulation sciences, and the growing preference for bio-based and eco-friendly products further reinforce its position in the global market. Lastly, government initiatives supporting the utility adjuvant market amid current market conditions are expected to continue boosting the industry.

The extensive agricultural landscapes of countries such as France, Germany, Spain, and Italy have created opportunities for farmers to use more crop protection products and tank mix adjuvants. The widespread adoption of precision farming and crop management practices has greatly increased the demand for tank mix adjuvants. Additionally, the growing preference for bio-based, environmentally friendly products has supported the sustainable use of pesticides and crop protection solutions. The rapid innovation in specialty chemicals and agrochemicals has positioned Europe as a leading region in the tank mix adjuvants market.

Leading Agriculture Utility Adjuvants Companies:

The report profiles key players such as BASF SE, Corteva Agriscience, Croda International Plc, Evonik Industries AG, Solvay SA, Nufarm Ltd., Dow Inc., Clariant AG, Huntsman Corporation, Helena Agri-Enterprises LLC, Wilbur-Ellis Company LLC, Stepan Company, Brandt Consolidated Inc., Akzo Nobel N.V., and Adjuvant Plus Inc.