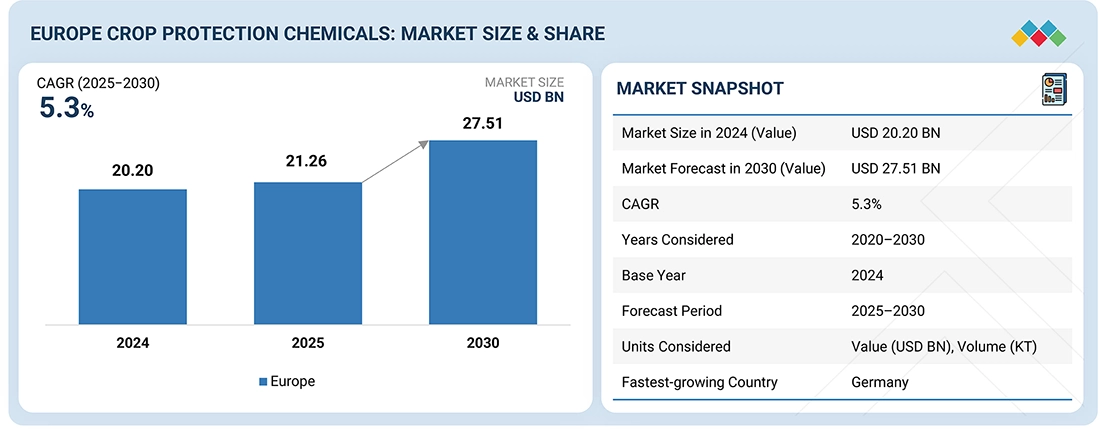

According to MarketsandMarkets™, the Europe crop protection chemicals market is projected to grow from USD 21.26 billion in 2025 to USD 27.51 billion by 2030, registering a Compound Annual Growth Rate (CAGR) of 5.3% during the forecast period. Market expansion is being driven by rapid technological innovation, rising demand for high-quality agricultural produce, and the increasing adoption of sustainable farming practices across the region.

Growth is strongly aligned with the European Union’s Green Deal objectives, with integrated pest management (IPM) programs, bio-based formulations, and residue-free crop protection solutions gaining momentum. Government initiatives supporting agricultural modernization, combined with the rising use of liquid formulations and microbial-based products, are accelerating market development. Increased investment in research and development—particularly in environmentally responsible crop protection technologies—is creating new opportunities for innovation, competitiveness, and long-term sustainability across Europe’s agricultural landscape.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=190542011

Herbicides Dominate the Type Segment

Herbicides are expected to account for a significant share of the European crop protection chemicals market. Their critical role in weed management for major crops such as cereals, oilseeds, and pulses continues to make them indispensable to both conventional and conservation tillage systems. Ongoing innovation in selective and broad-spectrum herbicide formulations, low-dose combination products, and precision agriculture integration is enhancing efficiency while reducing environmental impact. The continued adoption of integrated weed management practices further reinforces herbicides’ dominance, driven by their reliability, performance consistency, and compatibility with advanced application technologies.

Soil Treatment Gains Strong Momentum

The soil treatment segment is projected to hold a substantial share among application modes during the forecast period. Soil-applied fungicides, insecticides, fumigants, and bio-based solutions are increasingly adopted to improve soil health, control soil-borne diseases and nematodes, and enhance nutrient availability and root development. With growing demand for high-value crops and precision agriculture practices, controlled-release formulations and integrated soil management approaches are strengthening soil treatment’s role as a cornerstone of sustainable productivity in European farming systems.

Germany Emerges as a Strategic Market Leader

Germany is estimated to account for a significant share of the European crop protection chemicals market. The country’s large cultivation areas of cereals, oilseeds, and sugar beets, combined with a strong commitment to sustainable agriculture, are driving the adoption of environmentally responsible crop protection solutions. Increasing use of IPM systems, digital monitoring platforms, precision agriculture technologies, and bio-based formulations is positioning Germany as an innovation hub for the region. Strong regulatory alignment with EU environmental standards and continuous investment in sustainable technologies further reinforce its leadership role in the European market.

Leading Europe Crop Protection Chemicals Companies:

The report profiles key players such as BASF SE (Germany), Bayer AG (Germany), FMC Corporation (US), Syngenta Group (Switzerland), Corteva (US), UPL (India), Nufarm (Australia), Sumitomo Chemical Co., Ltd (Japan), Albaugh LLC (US), Koppert (Netherlands), Gowan Company (US), American Vanguard Corporation (US), Kumiai Chemical Industry Co., Ltd (Japan), PI Industries (India), and BioFirst Group (Belgium).