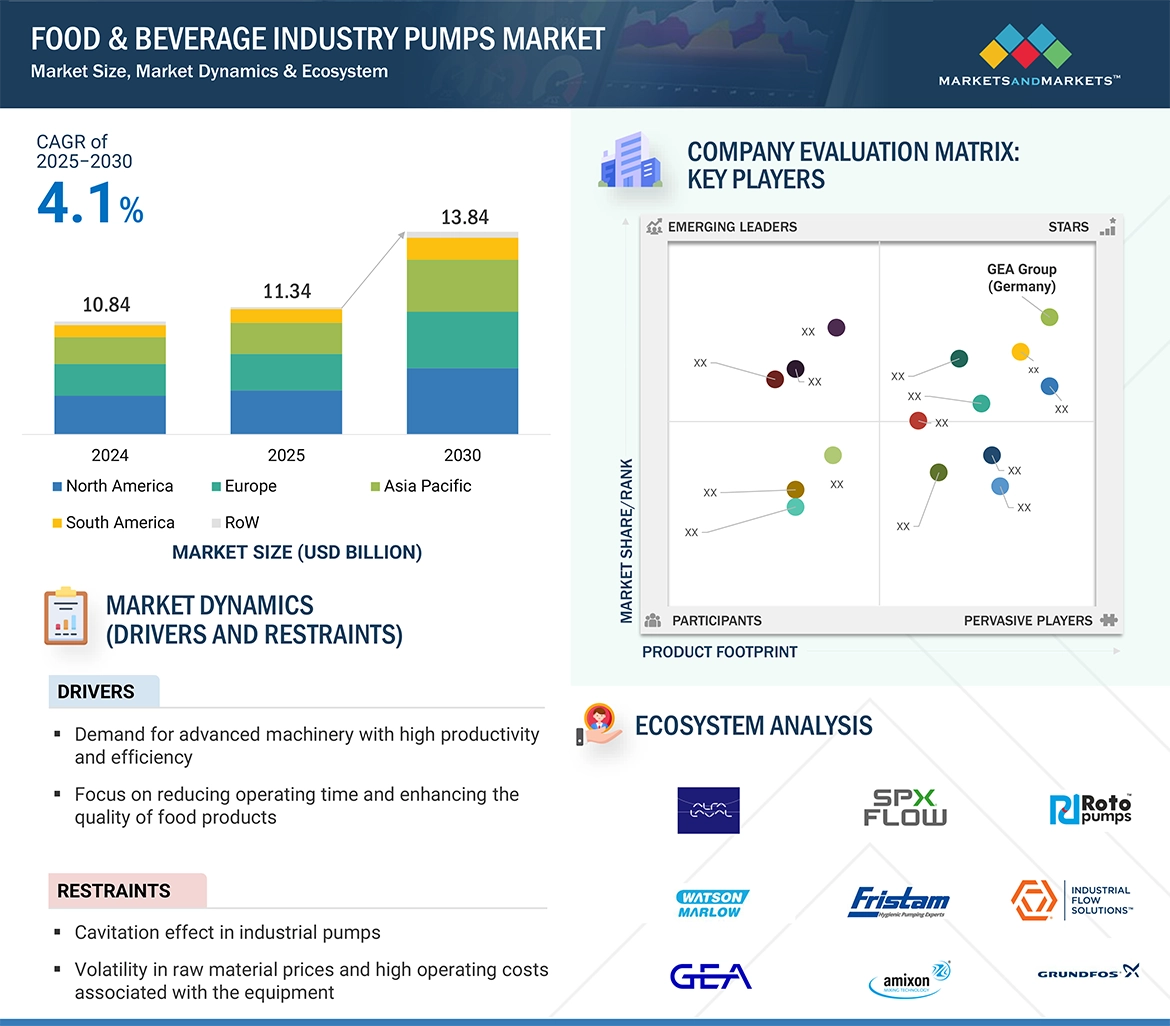

The food and beverage industry pumps market is projected to grow from USD 11.34 billion in 2025 to USD 13.84 billion by 2030, at a CAGR of 4.1% during the forecast period. This growth is driven by the increasing consumer demand for diverse food products, including plant-based and specialty items, necessitating advanced pumping systems capable of handling various ingredient viscosities and properties. These systems ensure efficient processing while maintaining product quality. Additionally, rising concerns over hygiene and contamination control in food processing are accelerating investments in sanitary pumps. Innovations in touch-free cleaning, bacteria-resistant materials, and high-standard hygiene solutions are shaping the competitive landscape of the industry.

Food & Beverage Industry Pumps Market Trends

The food & beverage industry pumps market is witnessing significant growth, driven by technological advancements, regulatory requirements, and evolving consumer demands. Below are some key trends shaping the market:

- Increased Demand for Hygienic and Sanitary Pumps: Food safety regulations and consumer preferences for high-quality, contamination-free food products are pushing manufacturers to invest in hygienic and sanitary pump solutions. Stainless steel, CIP (Clean-in-Place), and SIP (Sterilize-in-Place) pumps are becoming the industry standard.

- Growth in the Plant-Based and Specialty Food Segments: The rising demand for plant-based, organic, and specialty foods has led to the development of pumps that can handle viscous and delicate ingredients without compromising product integrity. This includes specialized pumps for dairy alternatives, protein-based beverages, and natural fruit fillings.

- Adoption of Smart Pump Technologies: The integration of IoT (Internet of Things), automation, and AI is revolutionizing pump systems. Smart pumps with real-time monitoring, predictive maintenance, and energy-efficient operations are gaining traction, reducing downtime and operational costs for food manufacturers.

- Focus on Energy-Efficient and Sustainable Solutions: Manufacturers are prioritizing eco-friendly and energy-efficient pumping systems to reduce their carbon footprint. Pumps with variable frequency drives (VFDs) and optimized energy consumption are becoming essential for sustainability goals in the food & beverage industry.

- Expansion of Cold Chain and Dairy Processing: With the rising demand for dairy, frozen foods, and cold beverages, the market for high-performance and temperature-resistant pumps is growing. These pumps are designed to handle refrigerated and frozen products efficiently.

- Rising Investments in Food & Beverage Infrastructure: The expansion of food processing facilities and beverage production plants worldwide is driving the demand for advanced pumping solutions. Developing markets, especially in Asia-Pacific and Latin America, are witnessing increased investments in modern food processing systems.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=211704387

Alcoholic Beverages has a significant share within the Application of the food & beverage industry pumps market.

The global demand for alcoholic beverages is rising, driving the need for highly efficient production processes. The manufacturing of beer, wine, spirits, and ready-to-drink cocktails requires large-scale fluid transfer across various stages, including fermentation, filtration, and bottling. Pumps play a critical role in handling different viscosities, alcohol concentrations, and carbonation levels, ensuring the safe and contamination-free movement of liquids.

For example, in beer production, pumps transfer wort through multiple processing stages, including filtration. In winemaking, they facilitate the gentle transfer of wine between barrels while leaving sediment behind. The expansion of craft breweries, microbreweries, and premium spirits brands has further increased the demand for specialized pump designs catering to both large-scale and artisanal production.

Additionally, stringent food safety and hygiene regulations in the alcoholic beverage industry are driving the adoption of sanitation-focused pump solutions. These pumps are designed for easy cleaning and maintenance while ensuring compliance with industry standards. The combination of increasing demand, operational efficiency, and regulatory requirements is fueling the growth of the pump market within the alcoholic beverage sector.

North America Dominates the food and beverage industry pumps market share.

Some key names such as JBT (US), Graco Inc. (US), Wastecorp Pumps (US), Sonic Corporation (US), Unibloc Hygienic Technologies US LLC (US), Ampco Pumps Company (US), Industrial Flow Solutions (US) and SPX FLOW (US)et al., all manufacture a plethora of pumps that meet diverse production techniques across the countries. They manufacture pumps that will handle all liquids and ingredients while assuring quality, hygiene, and performance in the pumping and processing of foods and drinks.

The U.S. houses the largest number of food and beverage manufacturing facilities. According to the reports from the U.S. Department of Agriculture in January 2025, these establishments accounted for 16.8 % of total manufacturing sales and 15.4 % of manufacturing employment in 2021. The largest group among these industries is meat processing, whose sales accounted for 26.2% in 2021, followed by dairy articles such as cheese and condensed milk (12.8%), other foods (12.4%), beverages (11.3%), and grains and oilseeds (10.4%). Meat processing, including livestock and poultry slaughter, remains the major contributor to pump demand because of the high volume involved and the complexity of processing in factories.

The boosting demand for advanced pumping systems for hygienic and contamination-free processing is an inevitable hallmark of an expanding food manufacturing sector and the increasing rigors of food safety standards in North America from time to time, along with a growing production capacity. So, the market share of the region remains huge and increasing within the food & beverage industry pumps segment.

Top 10 Companies in the Food & Beverage Industry Pumps Market

- GEA Group (Germany)

- ALFA LAVAL (Germany)

- KSB SE & Co. KGaA (Germany)

- JBT (US)

- Atlas Copco (Sweden)

- Graco Inc. (US)

- Grundfos Holding A/S (Denmark)

- Verder Liquids (Netherlands)

- PCM (France)

- Roto Pumps Limited (India)