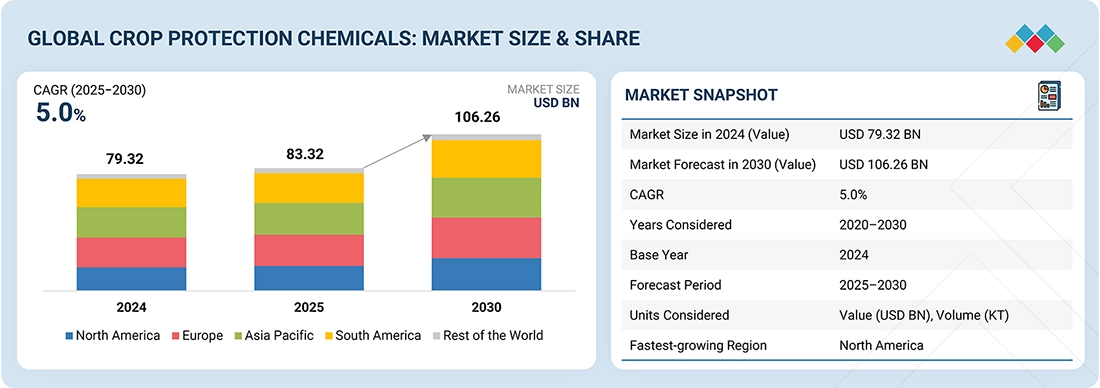

The crop protection chemical market is estimated at USD 83.32 billion in 2025 and is projected to reach USD 106.26 billion by 2030, at a CAGR of 5.0% from 2025 to 2030. The advancement of global trade in agricultural commodities has created a lot of pressure upon the farmer to meet stringent quality, appearance, and phytosanitary standards that would invariably increase the use of crop protection products. Agricultural labor shortages in several parts of the world have accelerated the trend toward chemical solutions as cheaper and easily scalable alternatives to manual weed and pest control. The organized retail, contract farming, and food processing industries are creating more and stronger demand for uniform, residue-compliant produce, indirectly facilitating continued adoption of crop protection chemicals across the global agriculture value chain.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=380

The synthetic crop protection chemicals segment holds the highest market share, by origin

Synthetic products hold the highest share in the origin segment of the crop protection chemical market, primarily due to their proven efficacy, broad-spectrum activity, and consistent performance across diverse crops and agro-climatic conditions. In particular, they are able to deliver both quick and reliable control levels of weeds, pests, and diseases. Thus, synthetic herbicides, fungicides, and insecticides are considered the best options in agro-commercial and large-scale farming systems. The highly standardized manufacturing processes, extended shelf life, and compatibility with modern applications provide features that favor developed countries and commercial farms for their usage. In addition, on the entire hectare basis of coverage, synthetic chemistry typically has a more economical response to the costs involved, which is important for farmers who want to get as much yield as possible while controlling input costs.

The soil treatment segment holds a significant share in the market, by mode of application

Soil treatment holds a significant share in the mode of application segment, as it combats key problems caused by soil-borne pathogens, nematodes, and root diseases that impact crop establishment and yield. The use of crop protection chemicals in soil drenching, seed bed treatment, and root-zone application supports better microbial colonization and long-term protection. Organic practices that enhance soil health, improve nutrient uptake, and minimize early-stage crop losses have found wide acceptance in horticulture, row crops, and protected cultivation systems.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=380

Based on region, Asia Pacific holds a large share in the crop protection chemical market.

The Asia Pacific region holds a significant share of the crop protection chemical market due to its vast agricultural base, high cropping intensity, and strong reliance on agriculture for food security and rural livelihoods. Important staple crops, mainly rice, wheat, maize, and pulses, which are produced largely on a global scale, do require regular management pertaining to weeds, pests, and diseases. Smallholder-style dominant farming systems, varied cropping cycles, and year-round cultivation in many countries increase the frequency of crop protection chemical use. Besides, rapid population increases and rising food consumption drive governments and farmers to focus on yield stability and loss prevention. Enhancing access to crop protection inputs, strengthening distribution networks, and increasing adoption of modern farming practices tend to offer great demand across key markets, including China, India, Southeast Asia, and Australia.

Leading Crop Protection Chemicals Companies:

The report profiles key players such as BASF SE (Germany), Bayer AG (Germany), FMC Corporation (US), Syngenta Group (Switzerland), Corteva (US), UPL (India), Nufarm (Australia), Sumitomo Chemical Co., Ltd (Japan), Albaugh LLC (US), Koppert (Netherlands), Gowan Company (US), American Vanguard Corporation (US), Kumiai Chemical Industry Co., Ltd (Japan), PI Industries (India), and BioFirst Group (Belgium).