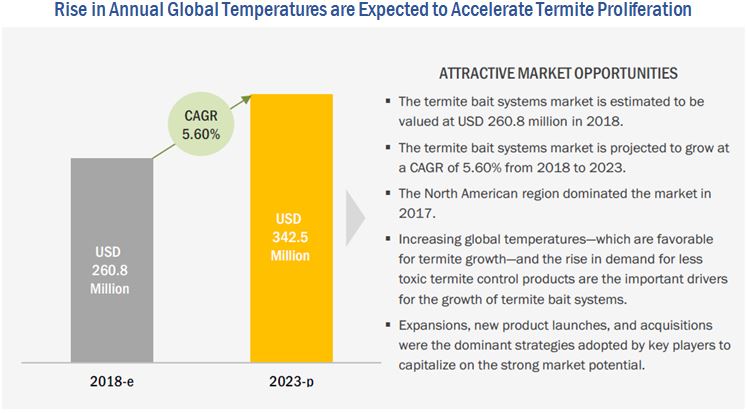

The report “Termite Bait Systems Market by Termite Type (Subterranean, Dampwood, Drywood), Station Type (In-Ground, Above-Ground), Application (Commercial & Industrial, Residential, Agriculture & Livestock Farms), and Region – Global Forecast to 2023″ The termite bait systems market is estimated to be USD 260.8 million in 2018 and is projected to reach USD 342.5 million by 2023, at a CAGR of 5.60% from 2018. The market growth is driven by factors such as increasing demand from customers for less-toxic pest control methods and increasing prevalence of termite-related infestations with respect to rising global temperatures.

In-ground bait stations are estimated to be the most widely used station type during the forecast period.

Subterranean termites are the most common termites present globally and cause the most destructive damage to houses and other properties. Since subterranean termites are found below ground level, in-ground termite bait stations are used to control these termite infestations. The in-ground segment accounted for 72.5% of the global termite bait systems market in 2017, in terms of station type.

The commercial & industrial segment is projected to be the fastest-growing during the forecast period.

The commercial & industrial segment is projected to register the highest growth rate from 2018 to 2023. The increasing commercial and industrial construction activities, especially in the developing regions, have led to an increased demand for termite control services. The commercial & industrial sector needs to adhere to certain hygiene standards. This can create a significant demand for pest and termite control services in and around commercial and industrial areas. Additionally, the need for less-toxic termite control methods, such as termite baits, is also expected to gain importance in the coming years from the commercial & industrial segment.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=211702476

North America is projected to dominate the market, while Asia Pacific is projected to be the fastest-growing market for termite bait systems through 2023.

The North American region accounted for the largest share in 2017 due to the presence of players such as DowDuPont (US), BASF (Germany), and Rentokil (UK). Moreover, the presence of these companies in technologically advanced countries such as the US and Canada, and higher consumer awareness about and preference for pest control services have been key factors for the increasing adoption of bait systems for termite control.

The market for termite bait systems in the Asia Pacific region is projected to grow at the highest CAGR from 2018 to 2023, owing to the increasing investments in the commercial & industrial sectors.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies. It also includes the profiles of leading companies such as DowDuPont (US), BASF (Germany), Bayer (Germany), Sumitomo Chemical (Japan), Spectrum Brands (US), PCT International (Australia), Syngenta (Switzerland), Rentokil Initial (UK), Ensystex (US), Rollins (US), Terminix International (US), and Arrow Exterminators (US).