The global plant genomics market is estimated to be valued at USD 7.3 billion in 2019 and is projected to reach USD 11.7 billion by 2025, recording a CAGR of 8.3%. The plant genomics market has high potential in emerging markets, such as Asia Pacific, due to the increasing awareness about the possible ill-effects of GM crops or food products in developing countries.

By trait, the plant genomics market is segmented into herbicide tolerance, disease resistance, yield improvement, and others. According to industry experts from prominent seed manufacturers, disease resistance and herbicide tolerance are the traits that have been on demand, owing to the increasing instances of early germination pest attacks and regulations against crop protection chemicals.

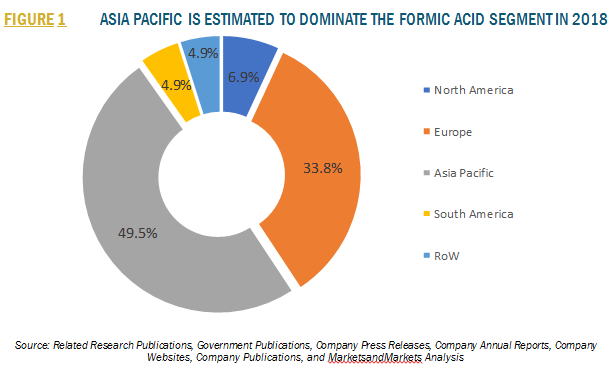

To know about the assumptions considered for the study download the pdf brochure

Based on application, the plant genomics market is segmented into cereals & grains, oilseeds & pulses, fruits & vegetables, and others. Among cereals & grains, rice, wheat, and corn are majorly bred using plant breeding & sequencing techniques, to develop high-performing varieties. Rice, along with wheat and corn, underpins the global food supply. Field crop science (including breeding, pathology, and economics) has contributed to a steady increase in crop productivity from decades through the availability of better varieties and hybrids with more effective pest and disease control and better production capacities. Molecular engineering technique development for genetic analysis has led to a great upsurge in the knowledge of cereal genetics and understanding of the structure and behavior of cereal genomes.

Based on objectives, the plant genomics market is segmented into DNA/RNA sequencing, genotyping, market-assisted selection, gene expression profiling, GMO-trait purity testing, DNA extraction & purification, and other objectives. DNA/RNA sequencing is estimated to be the most popular service required in the plant genomics market. The increasing number of samples tested per machine run due to efficient technological developments have encouraged companies to offer these services at cheaper costs. A common trend witnessed for basic information sequencing in the agricultural industry and among research professionals is to identify common markers such as plant height for breeding purposes. However, with the evolution of plant genomics research, the demand for genotyping tests is projected to surpass the demand for other objectives by 2025.

By type, the plant genomic market is divided into molecular engineering, genetic engineering, and others. The major plant breeders such as Bayer (Germany), Monsanto (US), DowDuPont (US), and BASF (Germany) have invested in plant breeding and been developing seed traits based on molecular breeding and genetic engineering techniques. Moreover, the favorable regulatory environment for GM crops in the US has encouraged plant breeders to adopt biotechnological methods at a larger scale in the country. The use of genetic engineering techniques for corn and soybean breeding is the highest in the US, while the adoption of molecular breeding techniques in Canada has been slowly rising.

The major players, such as Eurofins Scientific (Luxembourg), Agilent Technologies (US), and Illumina, Inc. (US) in the plant genomics market are focusing on new product launches, expansions & investments, acquisitions & mergers, agreements, joint ventures, collaborations, and partnerships to expand their global footprint.