The report “Taste Modulators Market by Type (Sweet Modulators, Salt Modulators, and Fat Modulators), Application (Confectionery Products, Bakery Products, Dairy Products, Snacks & Savory Products, and Meat Products), and Region – Global Forecast to 2023″, The global taste modulators market is estimated at USD 1,084.2 million in 2018 and is projected to reach USD 1,758.7 million by 2023, at a CAGR of 10.2% during the forecast period. The market is driven by factors such as the growing awareness among consumers about the ill-effects of excessive salt intake and the increased consumer demand for low-calorie products while retaining the original taste. There has been an increasing demand for reduced/zero calorie and reduced salt products that do not compromise on the taste. This has fueled the demand for taste modulators as well.

The sweet modulators segment, by type, estimated to account for the largest market share in 2018

The sweet modulators segment is estimated to dominate the global taste modulators market in 2018. Sweet modulators provide a sweet taste with zero calories to food products. It is used by manufacturers to restore the sweet taste. Taste modulators are gaining popularity among consumers owing to enhanced taste and nutritional benefits.

The beverages segment, by application, is estimated to hold a larger share in 2018.

Beverages are broadly classified into two categories, namely, alcoholic and non-alcoholic beverages. The non-alcoholic beverages segment was the largest; it includes both carbonated drinks and non-carbonated beverages such as juices, energy drinks, sports drinks, and fortified drinks. Taste modulators are used to alter the taste and support the reduction of calories in drinks (being used in conjunction with sugar substitutes) to meet consumer demand for healthy beverage products.

The Asia Pacific market is projected to grow at the highest CAGR from 2018 to 2023.

The Asia Pacific region is expected to grow at the highest CAGR during the forecast period. China and India have witnessed major growth in the taste modulators market, acquiring significant shares in the region. The region witnesses a high demand for taste modulators due to the rise in meat consumption, population growth, and increase in awareness about healthy & nutritional food products.

This report includes a study of various taste modulators, along with the product portfolios of leading companies. It includes the profiles of leading companies such as DSM (Netherlands), Kerry (Ireland), Ingredion (US), Givaudan (Switzerland), and Firmenich (Switzerland).

The global industrial hemp market size is projected to grow from USD 4.6 billion in 2019 to USD 26.6 billion by 2025, recording a compound annual growth rate (CAGR) of 34.0% during the forecast period. Rising awareness among the consumers about the benefits of industrial hemp, increasing legalization to cultivate industrial hemp across different countries, and growing application scope of industrial hemp in diverse industries such as textile, pharmaceutical, food, beverages, personal care products, construction & material, furniture, and paper is driving the market for industrial hemp.

Key industrial hemp players include Hempco (Canada), Ecofibre (Australia), Hemp Inc. (US), GenCanna (US), HempFlax BV (Netherlands), Konoplex Group (Russia), Hemp Oil Canada (Canada), BAFA (Germany), Hemp Poland (Poland), Dun Agro (Netherlands), Colorado Hemp Works (US), Canah International (Romania), South Hemp Tecno (Italy), Plains Industrial Hemp Processing (Canada), and MH Medical Hemp (Germany). Agreements, joint ventures, and partnerships were the dominant strategies adopted by major players, followed by expansion. These strategies have helped them to increase their presence in different regions.

Hempco, a subsidiary of Aurora Cannabis (Canada), is one of the leading manufacturers of cannabis products. Hempco is engaged in the processing of hemp-based products, such as hemp protein, hemp seed oil, and hemp fiber. It has developed a S.A.F.E soil program to provide chemical-free hemp crop and hemp-based products to consumers while achieving sustainable growth. The company strategies to capture the growing industrial hemp market all over the world. For instance, in March 2018, Hempco signed an agreement with Kane Veterinary Supplies, to supply its hemp-based animal supplements for pets and equine. This helped the company to capture the growing hemp-based animal health market in Canada.

Hemp Inc. (US) produces hemp-based products such as loss circulation material and absorbent used as a drilling fluid and to control oil spill, respectively. The company has nine divisions—the industrial hemp infrastructure, the hemp farming infrastructure, the hemp extraction infrastructure, the hemp educational infrastructure, accessories, products and services, research and development, industrial hemp investments and joint venture, and industrial hemp consulting. The company aims to provide hemp-based eco-friendly products to produce natural, sustainable products for worldwide markets, which can replace petroleum-based products. Through various joint ventures and agreements, the company strategies to expand its presence and product portfolio in the US. For instance, in January 2019, it formed a joint venture with Hemp Healthcare (US) to sell high-end CBD and hemp-based products.

The report Bovine Serum Albumin Market is estimated to be valued at USD 255 million in 2019 and is projected to reach a value of USD 304 million by 2025, growing at a CAGR of 3.0% during the forecast period. Factors such as the inexpensive and stable nature of bovine serum albumin as a protein standard, growing demand for blood-based products are some of the factors driving the growth of the market.

Objectives of the Report:

To define, segment, and project the global market size of the bovine serum albumin market

To understand the bovine serum albumin market by identifying its various subsegments

To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and industry-specific challenges)

To analyze the micromarkets, with respect to individual growth trends, prospects, and their contribution to the total market

To project the size of the market and its submarkets, in terms of value, with respect to the regions (along with their respective key countries)

To profile the key players and comprehensively analyze their core competencies

To understand the competitive landscape and identify the major growth strategies adopted by the players across the key regions

To analyze the competitive developments such as expansions & investments, mergers & acquisitions, new product launches, partnerships, joint ventures, and agreements

The Asia Pacific region holds a range of opportunities for pharmaceutical firms and multinational drugmakers. In the Asia Pacific region, China is the largest market for pharmaceutical products. With the growing interest in health and welfare, the demand for pharmaceutical products is growing. This would help drive the growth of BSA in this region.

Key Market Players:

The key players in this market include Thermo Fisher Scientific (US), Merck KGAA (Germany), Proliant Biologicals (US), Itoham Yonekyu Holdings Inc (Japan), and Bio-Rad Laboratories, Inc (US). Major players in this market are focusing on increasing their presence through new product launches, expansions & investments, and mergers & acquisitions. These companies have a strong presence in North America, Europe, and Asia Pacific. They also have manufacturing facilities along with strong distribution networks across these regions.

Theshelf-life testing market, by parameter, is estimated to be dominated by the microbial contamination segment and is also projected to be the fastest-growing. Microorganisms pose serious health problems, resulting in strict regulations imposed by national governments and international bodies with respect to maximum content levels in food products. As a result, shelf-life testing is essential to ensure that the microbial content in the food product is limited to only a certain level throughout its shelf life, thereby contributing to consumer safety and complying with regulatory limits.

The packaged food segment, by food tested, is estimated to dominate the market during the forecast period. Rapid urbanization has led to changes in consumer lifestyles. Higher employment opportunities and increased disposable incomes have led to increased consumption of packaged food products, which has, in turn, necessitated shelf-life testing for these products.

Key Players of the Market:

• SGS (Switzerland), • Bureau Veritas (France) • Intertek (UK) • Eurofins (Luxembourg) • ALS Limited (Australia) • TÜV SÜD (Germany) • TÜV NORD GROUP (Germany) • Mérieux (US)

The shelf-life testing market, by technology, is projected to be dominated by the equipment- & kit-based segment and is also projected to grow at a higher rate during the forecast period. This segment consists of both, traditional and rapid systems, which are highly preferred by manufacturers because of their ability to provide faster and more reliable results.

The Asia Pacific market is projected to grow at the highest CAGR from 2018 to 2023. Growth in the Asia Pacific region can be attributed to factors such as growth in the number of shelf-life testing laboratories in India and China, the rise in the number of incidences of bacterial infectious diseases in the region, and growing adoption of convenience and packaged food on the region.

The report “Top 10 Food Safety Testing and Technologies Trends(Food Safety, GM Food Safety, Food Pathogen, Meat Speciation, Food Authenticity, Pesticide Residue, Mycotoxin, Allergen, Water, and Bottled Water) – Global Forecast to 2022″, The top 10 food safety testing and technologies market is projected to reach USD 39.47 Billion by 2022.

The food safety testing and technologies market encompasses a variety of testing technologies. The markets covered under food safety testing include food safety testing market, GM food safety testing market, food pathogen testing market, meat speciation testing market, food authenticity testing market, pesticide residue testing market, mycotoxin testing market, and food allergen testing market. The markets covered under water safety testing & technologies include water testing and analysis and bottled water testing.

Implementation of Stringent Food Safety Regulations

Globalization of Food Supply

Availability of Advanced Technology Capable of Rapid Testing

Media Influence on Consumer Awareness About Food Safety

The global mycotoxin testing market is projected to grow at a CAGR of 6.0% to reach a value of USD 1.56 billion by 2022. Growth in awareness of consumers with regard to food safety is the most important driver for this market. There have been several food recalls due to the presence of mycotoxin in the food products resulting in increased attention toward this market. Government regulations also play a major driver in this market as several countries have stringent government regulations and there are regulatory authorities that check if the food product is free from mycotoxins and fit for human and animal consumption.

This report includes a study of marketing and development strategies, along with the product portfolios of the leading companies. It includes profiles of leading companies such as SGS S.A. (Switzerland), Bureau Veritas S.A. (France), Intertek Group plc (U.K.), Eurofins Scientific SE (Luxembourg), ALS Limited (Australia), Thermo Fisher Scientific Inc. (U.S.), Mérieux NutriSciences Corporation (U.S.), AsureQuality Ltd. (New Zealand), Microbac Laboratories Inc. (U.S.), and Romer Labs Diagnostic GmbH (Austria).

The bleaching agents market is estimated at USD 728.6 Million in 2018 and is projected to reach USD 953.8 Million by 2023, growing at a CAGR of 5.5% during the forecast period. This market is driven by factors such as the increase in the consumption of bread and related bakery products along with advancements in technology for flour evaluation.

Scope of the Report:

On the basis of Type, the market for bleaching agents has been segmented as follows:

Azodicarbonamide

Hydrogen peroxide

Ascorbic acid

Acetone peroxide

Chlorine dioxide

Others (chlorine, benzoyl peroxide, calcium peroxide, and sulfur dioxide)

On the basis of Form, the market for bleaching agents has been segmented as follows:

Powder

Liquid

On the basis of Application, the market for bleaching agents has been segmented as follows:

Bakery products

Flour

Cheese

Others (sugar, candies, and caramel)

On the basis of Region, the market for bleaching agents has been segmented as follows:

The flour segment, by application, accounted for the largest share of the market in 2017. Bleaching agents are used for whitening flour, as freshly milled flour has a slightly yellowish color as it contains carotenoids. Additionally, bleaching oxidizes the surface of the flour and promotes its gluten-producing potential. Bleaching of flour helps in the weakening of the proteins and maturation of the flour in a reduced amount of time and has thereby become a necessity for flour producers. Some of the most common flour bleaching agents include hydrogen peroxide, benzoyl peroxide, and chlorine dioxide.

Asia Pacific is projected to be the fastest-growing market for bleaching agents during the forecast period. The major countries with growth potential in this market include China, India, Japan, and Australia. India is estimated to account for a significant share of the Asia Pacific market through 2023. This is an emerging market and hence provides opportunities for the growth of the bleaching agents market.

The market for hydrocolloids is estimated at USD 8.8 billion in 2018 and is projected to grow at a CAGR of 5.3% from 2018 to 2023, to reach USD 11.4 billion by 2023. The growth of the hydrocolloids market is driven by the rising demand for convenience foods in the food industry. The key market drivers are the R&D activities and innovation, consumer preference for functional dairy products, and multifunctionality of hydrocolloids in food & beverage products.

Drivers

Rise in Consumption of Premium Food & Beverage Products

Multi-Functionality of Hydrocolloids Leads to Their Wide Range of Applications

Increase in Health-Consciousness Among Consumers Drives the Natural Hydrocolloids Market

Restraints

Stringent International Quality Standards and Regulations

Shortage of Resources has Created A Demand-Supply Imbalance

Opportunities

The Emerging Markets Illustrate Great Potential for Hydrocolloids

Increase in Investments in Research & Development

Challenges

Fluctuations in Prices of Raw Materials

Unclear Labeling Leading to Ambiguity and Uncertainty

The food & beverage segment, by application, is projected to be the largest revenue contributor in the hydrocolloids market during the forecast period.

The food & beverage segment is accounted to hold the largest share in the hydrocolloids market in 2018. Hydrocolloids are widely used in food products such as bakery, confectionery, meat & poultry, beverages, and dairy & frozen products. The growth of the hydrocolloids market is driven by the rising demand for convenience foods from the food industry.

The demand for thickeners segment, by function, is estimated to rise and dominate the hydrocolloids market during the forecast period.

In terms of function, thickeners and stabilizers were the most widely preferred functions for hydrocolloids. The market was dominated by the thickening segment and is used to maintain viscosity in the presence of electrolytes, high temperature, and wide pH ranges in food products such as soups & gravies, ketchup, instant beverages, desserts, toppings, and fillings. This thickening segment accounted for 40% of the market in 2017.

North America is projected to account for the largest market size during the forecast period.

North America is a dominant region in the global hydrocolloids market. Factors influencing its market dominance include the high demand for functional dairy products, convenience foods, higher per capita consumption of baked goods, and presence of major players.

This report includes a study of marketing and development strategies along with the product portfolios of leading companies in the hydrocolloids market. It includes profiles of leading companies such as Ingredion (US), Cargill (US), DowDuPont (US), Darling Ingredients (US), ADM (US), and Kerry (Ireland).

To define, segment, and project the global market size for omega-3

To understand the omega-3 market by identifying its various subsegments

To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and industry-specific challenges)

To analyze the micromarkets, with respect to individual growth trends, prospects, and their contribution to the total market

To project the size of the market and its submarkets, in terms of value, with respect to the regions (along with their respective key countries)

To profile the key players and comprehensively analyze their core competencies

To understand the competitive landscape and identify the major growth strategies adopted by the players across the key regions

To analyze the competitive developments, such as expansions & investments, mergers & acquisitions, new product launches, partnerships, collaborations, and agreements

In October 2019, KD Pharma (Germany) introduced Kardio3, which is a blend of omega-3, vitamin K2, and phytosterols. It aids in maintaining healthy lipids and supports heart and bone health.

In September 2019, Epax (Norway) announced an investment of USD 35 million over the next two years for the innovation of its Omega-3 sector. This investment will allow Epax to have better capacity in the omega-3 industry at its main site of production in Norway. It will facilitate the extended concentration of EPA and DHA without prompting oxidation, which will ultimately avoid unwanted by-products.

In September 2019, Polaris (France) launched Omegavie DHA 700 algae Sensory QualitySilver, which would help the company in the field of algal omega-3. The product majorly contains DHA and also contains excellent organoleptic properties.

Factors Influencing Global Growth:

Drivers

Consumer Awareness Regarding the Health Benefits of Omega-3

Increase in Application Profiling and Existing Applications Finding New Markets

Innovative Production Technologies

Restraints

Lower Fish Oil Supply Due to Sustainability Issues Among Fisheries

Lack of Clarity Among Consumers About Daily Recommended Intake

Opportunities

Research for the Development of Alternative Sources to Obtain Omega-3

Emerging Economies of Asia Pacific and South America to Witness High Growth

Favorable Regulatory Environment

Microencapsulation

Awareness About Certified Food Ingredients

Challenges

High Cost Involved in R&D Activities

Highly Unstable Fish Oil Prices

Monetary Growth Expectations, Globally:

The omega-3 market size is estimated to account for a value of USD 4.1 billion in 2019 and is projected to grow at a CAGR of 13.1% from 2019, to reach a value of USD 8.5 billion by 2025. Consumer awareness regarding the health benefits of omega-3 and an increase in application profiling and existing applications finding new markets are projected to drive the growth of the omega-3 industry.

The omega-3 market in Asia Pacific is projected to witness high growth due to rising awareness about its health benefits and increasing disposable income of the population in the Asia Pacific countries. With the growing inclination toward healthy aging in the region, the adult population prefers consuming dietary supplements, including omega-3, as per the recommendations by the Global Organization for EPA & DHA Omega-3 (GOED). Moreover, in Asia Pacific countries, the governments are also focusing on and promoting fortified foods, and many big brands such as BASF (Germany) and Croda International (UK) have expanded their operations in these countries to cater to the growing demand for omega-3. Key manufacturers prefer expanding in the Asia Pacific region, as it provides cost-effective benefits during production and processing. The high demand for omega-3 and low cost of production are the major factors that are projected to encourage suppliers and manufacturers to invest in this market. In addition, Asia Pacific has the highest growth potential due to factors such as high economic growth and the increase in income of individuals in the region. The high population growth and increase in FDI are factors that are driving the growth of the omega-3 market.

Consumers are focusing on having healthy lifestyles through the consumption of various fermented products that impart better gut health. Consumers’ perception about fermented products is rapidly growing as a result of the increasing health benefits provided by these products. The psychological health benefits provided by fermented products are gaining high traction among consumers through health claims that include immunity, cardiovascular, digestive, and slimming aids. Consumers are expecting a variety of new categories in fermented products that help promote sleeping and decrease internal body heat. For instance, fermented food producers have started the usage of probiotics in kombucha, a fermented tea drink, due to the increased health benefits offered. Hence, the increasing consumer focus on the consumption of fermented food products for various health claims is another factor to drive the growth of the fermenters market.

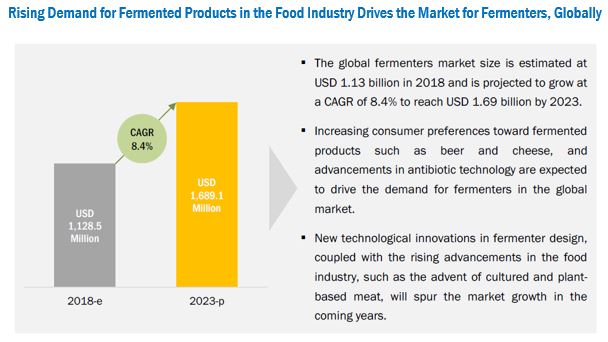

The global market for fermenters is projected to reach USD 1.68 billion by 2023, at a CAGR of 8.4%

The fermenters market is majorly driven by their application in food, beverages, and healthcare products & cosmetics. The market is driven by consumer awareness about the health benefits provided by fermenters; these include improved immunity, digestion, and weight management associated with fermented products. Fermenters are broadly used for producing microbial cultures that are used in the production of alcoholic fermentation of beverages, such as beers and wines. They are also used in food products such as yogurt, pickles, kombucha, tempeh, kimchi, bakery & related products, and antibiotics.

Rise in consumption of fermented beverages across the globe drives the growth prospects of fermenters

The rapidly growing fermented beverage industry is expected to dominate and drive the demand for fermenter systems and solutions during the forecast period, owing to the growing popularity of a variety of beers and wines in the emerging economies, worldwide. According to the Brewer’s Association, in 2017, the craft beer sales continued to grow at a rate of about 5%, by volume, which reached 12.7% of the US beer market. According to the TTB and US Commerce, 2018, the US domestically produced about 83% of the beer; and 17% of it was imported from more than 100 different countries. According to TTB preliminary reports, the US recorded about 5,648 brewery production facilities in the region in 2017. According to the Brewers of Europe Organization, in 2016, Germany, the UK, Poland, Spain, and the Netherlands recorded high growth in beer production. Thus, the growing popularity of beer among consumers is expected to lead to the exponential growth in demand for fermented beverages, thereby increasing the demand for fermenters used for alcoholic fermentation of these beverages. Hence, the beverages segment, by application, is projected to be the largest and fastest-growing market between 2018 and 2023.

Geographical Prominence

Asia Pacific is the fastest-growing region in the global economy. Fermentation advancements in the Asia Pacific food & beverage industry have resulted in more opportunities for the fermenters market. The region is expanding as a leading region in the production of a variety of probiotic-based foods, beverages, and dietary supplements. Innovations have also been reported in the dessert, confectionery, and fermented food sectors in the region. India is one of the fastest-growing markets for fermenters due to the increase in demand for fermented food, beverage, and healthcare products in the country.

Factors driving the growth of the Asia Pacific fermenter market are increase in awareness among consumers about fermented food products, rise in demand for cheese and related products among consumers, growing incidences of antibiotic-resistant infectious diseases—which has led to the demand for microorganisms or microbial strains using fermenters, growing health awareness, the rising demand for fortified fermented food products, and the increasing preference for natural products.

Factors driving the growth of the Asia Pacific fermenter market are increase in awareness among consumers about fermented food products, rise in demand for cheese and related products among consumers, growing incidences of antibiotic-resistant infectious diseases—which has led to the demand for microorganisms or microbial strains using fermenters, growing health awareness, the rising demand for fortified fermented food products, and the increasing preference for natural products.

Emerging economies such as India, Brazil, and Mexico have the favorable market potential for fermented food products, which has led food manufacturers in these countries to adopt strategies, such as expansions, to cater to the rising demand and use of fermenters to increase the production capacity of fermented products.

The major players in the fermenters market have adopted strategies, such as acquisitions, partnerships, investments, expansions, and agreements, to achieve growth. Companies are involved in major acquisitions and joint ventures that have strengthened their market positions in the fermenters market and expansion in their product portfolios and production capacity facilities.

Rise in demand and consumption for fermented food & beverages, such as cheese, beer, and wine, and the increasing awareness among the consumers relating to food preservation and benefits of the fermentation process are the major factors that are expected to fuel the growth of the fermenters market in the next coming years. The popularity of super premium beers and imported beers is increasing among the young population, given the increasing disposable income in developed economies. Furthermore, new technological innovations in fermenter design, coupled with the rising advancements in the food industry, such as the advent of cultured and plant-based meat, will spur the market growth in the coming years.

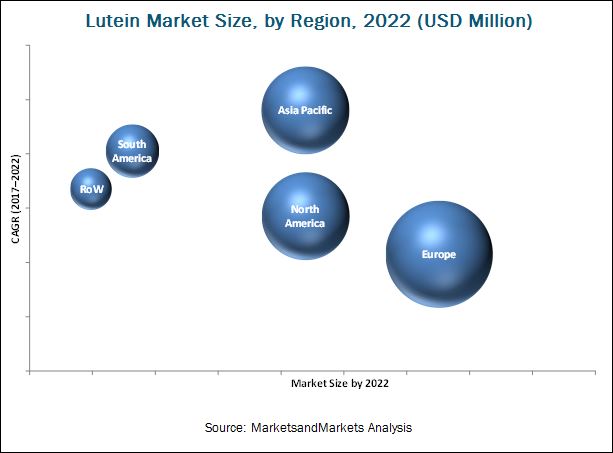

The report “Lutein Market by Form (Powder & Crystalline, Oil Suspension, Beadlet, Emulsion), Source (Natural, Synthetic), Application (Food, Beverages, Dietary Supplements, Animal Feed), Production Process, and Region – Global Forecast to 2022“, published by MarketsandMarkets™, The market for lutein, in terms of value, is estimated to be USD 263.8 Million in 2017, and is projected to reach USD 357.7 Million by 2022, at a CAGR of 6.3% from 2017.

The increase in demand for lutein as a natural colorant in food and beverage applications, rise in demand for eye health supplements, and the use of lutein in animal feed additives are expected to drive the demand for this ingredient in various consumer markets. Lutein plays a vital role in preventing age-related macular degeneration (AMD) disease. The Lutein Market, over the past few years, has been largely driven by the growing demand health supplements that contain lutein. Eye health supplements that contain lutein help preventing/curing eye diseases such as AMD and cataract. However, currently, the manufacturers are increasingly inclined to invest in other end-use applications and hence the market for dietary supplements application is growing at a lower rate when compared to applications such as food and beverages.

The dietary supplements segment expected to dominate the Lutein Market through 2022.

In 2016, the dietary supplements segment accounted for the largest share, by application, in the Lutein Market in terms of value and volume, as lutein is mainly associated with the eye health and is increasingly used as an ingredient in the eye health supplements.

Naturally sourced lutein is projected to be the faster-growing market during the forecast period.

The natural segment is projected to grow at a higher CAGR from 2017 to 2022. Growing awareness about the benefits of naturally obtained lutein and the increasing health conscious population leads to increased spending on high-quality lutein products, subsequently driving the market for naturally sourced lutein.

The emulsions segment is projected to be the fastest-growing segment in the Lutein Market from 2017 to 2022.

The demand for emulsion form of lutein is increasing around the globe, especially in developing countries such as China, India, and Brazil. Lutein emulsion is generally used in food and beverage applications and is currently used in cosmetics as well. Fortified food emulsion is widely used in the functional food segment wherein carotenoid-protein complex is used to prepare an emulsion. Leading players are gradually expanding their product range by developing lutein emulsion for the food industry. The emulsion segment is hence projected to be the fastest-growing segment in the Lutein Market from 2017 to 2022.

Asia Pacific is projected to be the fastest-growing regional market for lutein.

The Asia Pacific region is projected to be the fastest-growing market for lutein over the next five years, owing to increase in overall economic growth which has led to an increase in urbanization and rapid industrialization and subsequent growth in the consumer markets of China, India, Australia, and Japan.

In this region, countries such as India, China, and Japan hold a major share of more than 60% of the Asia Pacific Lutein Market. India is one of the fastest-growing markets for lutein in the Asia Pacific region. The changing lifestyle and preferences, increasing awareness regarding the benefits of lutein, the growth of the health-conscious population, higher disposable incomes, and growth of the middle-class population are some of the factors driving the growth of lutein the market in India.