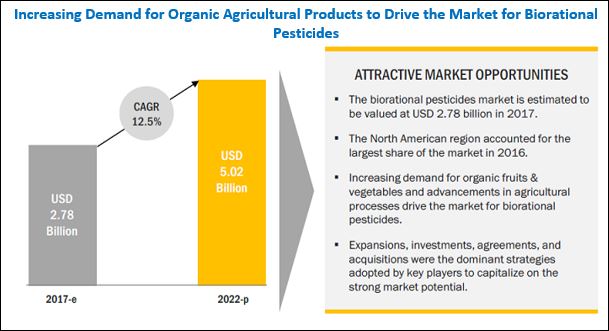

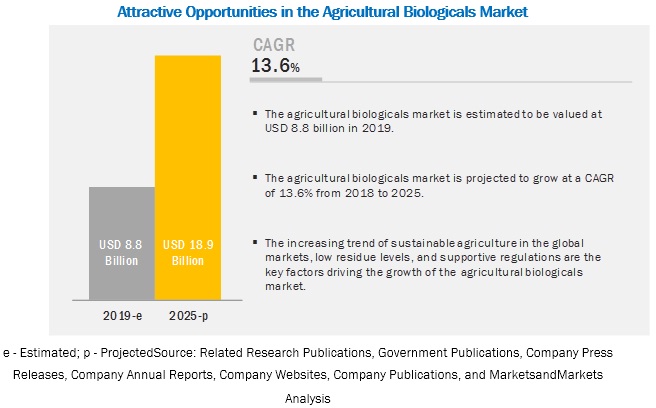

The agricultural biologicals market size is estimated to account for a value of USD 8.8 billion in 2019 and is projected to grow at a CAGR of 13.6% to reach a value of USD 18.9 billion by 2025. Factors such as the increasing trend of sustainable agriculture in the global market, low residue levels, and supportive regulations are the key factors driving the growth of the agricultural biologicals market. Expansions, new product launches, and agreements were the dominant strategies adopted by key players to capitalize on the strong market potential.

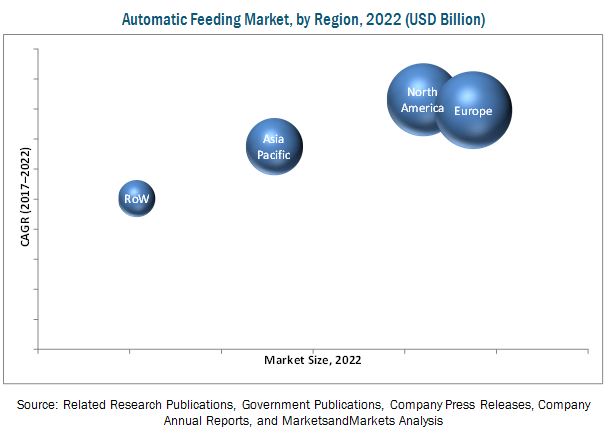

North America is projected to grow at the highest CAGR during the forecast period

The North American region accounted for the largest share in the market. This market is projected to grow at the highest CAGR during the forecast period. The largest share of the North American region is attributed to its high-end R&D infrastructure and the high number of patents received for biopesticides and biostimulants by companies based in the region.

This report includes a study on the marketing and development strategies, along with a survey of the product portfolios of the leading companies operating in the agricultural biologicals market. It includes the profiles of leading companies, such as BASF SE (Germany), Syngenta (Switzerland), Marrione Bio Innovation (US), Isagro (Italy), UPL (India), Evogene (Israel), Bayer (Germany), Vegalab (US), Valent (US), Stockton (Israel), Biolchim (Italy), Rizobacter (Argentina), Valagro (Italy), Koppert Biological Systems (Netherlands), Lallemand (Canada), Symborg (Spain), Andermatt Biocontrol (Switzerland), Seipasa (Spain), and Verdasien Life Sciences (US).

By function, the biocontrol segment is estimated to account for the largest market share, in terms of value

The product portfolio of major companies operating in the agricultural biologicals market is more focused on biocontrols due to the high demand for bioinsecticides and biofungicides for integrated pest management in developed countries. The major advantages of integrated pest management are that these are usually inherently less or not toxic than others affecting only the target pest and closely related organisms, effective in micro-quantities, and quickly kill.

The microbial segment, on the basis of product type, is estimated to account for the largest share in the agricultural biologicals market, in terms of value

The major market share of the microbials segment is attributed to the high usage of microbes in the production of biopesticides and biofertilizers, as they provide essential benefits to crops in terms of efficiency and productivity. Microbes are easy to find and cultivate on a large-scale.

Request for Customization: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=100393324

The foliar spray segment, on the basis of mode of application, is estimated to account for the largest share in the agricultural biologicals market, in terms of value

The agricultural biologicals market, by mode of application, was dominated by the foliar spray segment. Foliar application helps increase nutrient supply during the early growth stages when the root system is not well-developed. Also, the volume required for foliar application is low as compared to soil application. Farmers use the foliar mode of application to apply fertilizers on crops such as apple, grapes, pomegranate, and okra.

By crop type, the fruits & vegetables segment is estimated to account for the largest market share, in terms of value

The fruits & vegetables segment is projected to be the largest segment in the market. Fruits & vegetables are high-value crops and require higher nutrition during their growth stages. This is projected to drive the markets for biopesticides and biofertilizers, which are cheaper as compared to synthetic pesticides and fertilizers. In addition, farmers in the Asia Pacific, North American, and European regions are witnessing a rise in demand for organic agricultural products. This has encouraged the demand for agricultural biologicals in fruit & vegetable cultivation.