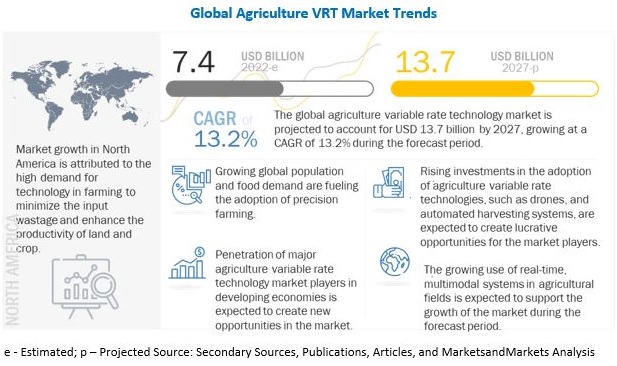

The agricultural industry has undergone a revolutionary change in recent years with the introduction of variable rate technology (VRT). The VRT is a modern farming technique that allows the farmers to vary the rate of input such as seeds, fertilizer, herbicide, and water according to the specific requirement of the field. The application of VRT in agriculture enhances crop production, reduces environmental impacts, and increases profitability by lowering input and application costs. The global agricultural variable rate technology (VRT) market is projected to reach USD 13.7 billion by 2027, recording a CAGR of 13.2% during the forecast period.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=178591689

Crop Type: Cereals & Grains to Dominate the Agriculture VRT Market

As per the statistics, cereals and grains are the largest crop type being harvested globally, with around 728 million hectares of land under cereal cultivation in 2018. Among various crop types, cereals such as corn, wheat, and rice have the highest adoption rate as they are majorly grown in large farms. The cereals & grains segment is projected to account for the largest growth in the agriculture variable rate technology market. The VRT allows input application rates to be varied across fields for site-specific management of the field variability. VRT helps in reducing input usage, thereby decreasing environmental impacts such as greenhouse gas emission, soil erosion & degradation, and genetic erosion.

Application Method: Sensor-Based VRT to Exhibit Fastest Growth

Sensor-based VRT is expected to account for the fastest growth in the agriculture variable rate technology market. Unlike map-based application methods, the sensor-based VRT does not require a map or positioning system. The sensor based VRT utilizes active optical sensors, drones, and satellite mapping for real-time site-specific management of the field variability. However, the high cost of these sensor based VRT systems could be a major concern during the forecast period.

Farm Size: Mid-Sized Farms to Grow Fastest

Mid-sized farms are expected to account for the highest growth rate during the forecast period. Agriculture VRT helps in increasing farmers’ profitability while preserving the environment with chemical fertilizers and crop protection chemicals. The increasing demand for food supply has led to high adoption of precision farming technologies in medium-sized farms in emerging countries.

Region: North America to Dominate the Market

North America is expected to dominate the agriculture variable rate technology market due to the increasing adoption of advanced technologies in various crops. The U.S. has more than 15% of farms that are more than 200 hectares and grows commercial crops that require these types of advanced technologies for profitable and efficient farming.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=178591689

Key Market Players

The key players in this market include Deere & Company, Trimble, Inc, AGCO Corporation, Topcon Corporation, CNH Industrial N.V., Kubota Corporation, Yara International, SJ DJI Technology Co., Ltd., Valmont Industries, Inc, Lindsay Corporation, and others.

Conclusion

The inclination of farmers toward maintaining the health of their crop and increasing productivity is driving the market for agricultural variable rate technology products. The adoption of VRT can help in reducing input usage and environmental impacts, increasing productivity and profitability, and preserving the environment. The VRT is a smart approach to farming that helps farmers to efficiently manage their field variability, thereby enhancing crop production.