Consumers are focusing on having healthy lifestyles through the consumption of various fermented products that impart better gut health. Consumers’ perception about fermented products is rapidly growing as a result of the increasing health benefits provided by these products. The psychological health benefits provided by fermented products are gaining high traction among consumers through health claims that include immunity, cardiovascular, digestive, and slimming aids. Consumers are expecting a variety of new categories in fermented products that help promote sleeping and decrease internal body heat. For instance, fermented food producers have started the usage of probiotics in kombucha, a fermented tea drink, due to the increased health benefits offered. Hence, the increasing consumer focus on the consumption of fermented food products for various health claims is another factor to drive the growth of the fermenters market.

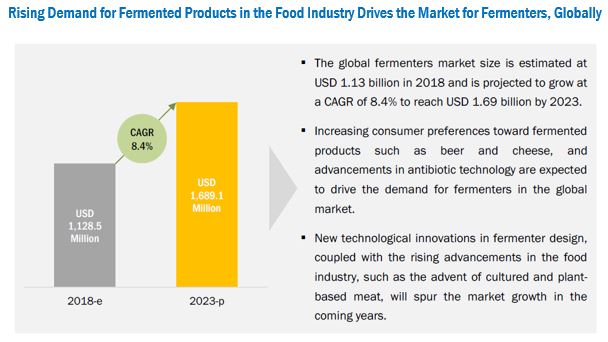

The global market for fermenters is projected to reach USD 1.68 billion by 2023, at a CAGR of 8.4%

The fermenters market is majorly driven by their application in food, beverages, and healthcare products & cosmetics. The market is driven by consumer awareness about the health benefits provided by fermenters; these include improved immunity, digestion, and weight management associated with fermented products. Fermenters are broadly used for producing microbial cultures that are used in the production of alcoholic fermentation of beverages, such as beers and wines. They are also used in food products such as yogurt, pickles, kombucha, tempeh, kimchi, bakery & related products, and antibiotics.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=101132363

Rise in consumption of fermented beverages across the globe drives the growth prospects of fermenters

The rapidly growing fermented beverage industry is expected to dominate and drive the demand for fermenter systems and solutions during the forecast period, owing to the growing popularity of a variety of beers and wines in the emerging economies, worldwide. According to the Brewer’s Association, in 2017, the craft beer sales continued to grow at a rate of about 5%, by volume, which reached 12.7% of the US beer market. According to the TTB and US Commerce, 2018, the US domestically produced about 83% of the beer; and 17% of it was imported from more than 100 different countries. According to TTB preliminary reports, the US recorded about 5,648 brewery production facilities in the region in 2017. According to the Brewers of Europe Organization, in 2016, Germany, the UK, Poland, Spain, and the Netherlands recorded high growth in beer production. Thus, the growing popularity of beer among consumers is expected to lead to the exponential growth in demand for fermented beverages, thereby increasing the demand for fermenters used for alcoholic fermentation of these beverages. Hence, the beverages segment, by application, is projected to be the largest and fastest-growing market between 2018 and 2023.

Geographical Prominence

Asia Pacific is the fastest-growing region in the global economy. Fermentation advancements in the Asia Pacific food & beverage industry have resulted in more opportunities for the fermenters market. The region is expanding as a leading region in the production of a variety of probiotic-based foods, beverages, and dietary supplements. Innovations have also been reported in the dessert, confectionery, and fermented food sectors in the region. India is one of the fastest-growing markets for fermenters due to the increase in demand for fermented food, beverage, and healthcare products in the country.

Factors driving the growth of the Asia Pacific fermenter market are increase in awareness among consumers about fermented food products, rise in demand for cheese and related products among consumers, growing incidences of antibiotic-resistant infectious diseases—which has led to the demand for microorganisms or microbial strains using fermenters, growing health awareness, the rising demand for fortified fermented food products, and the increasing preference for natural products.

Factors driving the growth of the Asia Pacific fermenter market are increase in awareness among consumers about fermented food products, rise in demand for cheese and related products among consumers, growing incidences of antibiotic-resistant infectious diseases—which has led to the demand for microorganisms or microbial strains using fermenters, growing health awareness, the rising demand for fortified fermented food products, and the increasing preference for natural products.

Emerging economies such as India, Brazil, and Mexico have the favorable market potential for fermented food products, which has led food manufacturers in these countries to adopt strategies, such as expansions, to cater to the rising demand and use of fermenters to increase the production capacity of fermented products.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=101132363

Conclusion

The major players in the fermenters market have adopted strategies, such as acquisitions, partnerships, investments, expansions, and agreements, to achieve growth. Companies are involved in major acquisitions and joint ventures that have strengthened their market positions in the fermenters market and expansion in their product portfolios and production capacity facilities.

Rise in demand and consumption for fermented food & beverages, such as cheese, beer, and wine, and the increasing awareness among the consumers relating to food preservation and benefits of the fermentation process are the major factors that are expected to fuel the growth of the fermenters market in the next coming years. The popularity of super premium beers and imported beers is increasing among the young population, given the increasing disposable income in developed economies. Furthermore, new technological innovations in fermenter design, coupled with the rising advancements in the food industry, such as the advent of cultured and plant-based meat, will spur the market growth in the coming years.