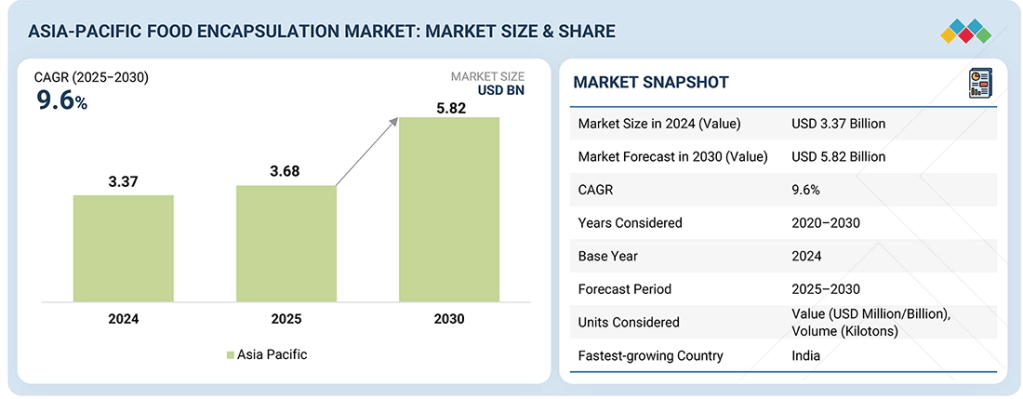

The Asia Pacific Food Encapsulation Market is projected to grow from USD 3.68 billion in 2025 to USD 5.82 billion by 2030, expanding at a Compound Annual Growth Rate (CAGR) of 9.6% during the forecast period. Food and nutrition companies across the region are increasingly adopting advanced encapsulation technologies to enhance ingredient stability, shelf life, bioavailability, and functional performance in food products. This technological shift is driving sustained market growth across applications, including functional foods and beverages, dietary supplements, infant nutrition, bakery, dairy, and confectionery products. Encapsulation enables controlled release, taste masking, and protection of sensitive ingredients from heat, moisture, and oxidation—making it a critical innovation platform for next-generation food formulations.

Growth is strongly supported by rising health awareness, rapid urbanization, expanding middle-class populations, and increasing demand for fortified and clean-label food products across key economies such as China, India, Japan, South Korea, and Southeast Asia. Advancements in formulation technologies—including spray drying, lipid-based systems, and nano-scale encapsulation approaches—are accelerating commercialization across the food sector. In parallel, supportive regulatory frameworks in food safety and nutrition fortification, combined with strong investments by regional and global ingredient suppliers in local manufacturing capacity and R&D, are strengthening market adoption. Preventive healthcare trends and the shift toward functional nutrition continue to stimulate product innovation and differentiation across the Asia Pacific food industry.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=245671954

Vitamins & Minerals Segment to Lead by Core Material

By core material, the vitamins & minerals segment is estimated to account for the largest market share.

These micronutrients are widely used in the fortification of staple foods, functional foods, and dietary supplements. Governments and public health authorities in countries such as India, China, Indonesia, and the Philippines are actively promoting micronutrient fortification to address deficiencies in iron, iodine, vitamins A and D, and folic acid.

Food encapsulation provides a protective matrix for fragile micronutrients, shielding them from thermal degradation, moisture exposure, oxidation, and processing losses, while ensuring uniform dispersion and extended shelf stability in mass-consumption products. Rising consumption of fortified dairy alternatives, cereals, beverages, and nutrition powders, along with increasing disposable incomes and preventive healthcare awareness among urban consumers, continues to fuel demand. For manufacturers, encapsulation enables regulatory compliance, consistent nutrient delivery, and clean-label positioning, making vitamins and minerals the most commercially dominant core materials in the regional market.

Polysaccharides to Dominate Shell Material Segment

By shell material, the polysaccharides segment is projected to hold the largest market share in Asia Pacific.

Polysaccharides—including starch derivatives, maltodextrins, alginates, gum arabic, and modified cellulose—are widely adopted due to their natural origin, regulatory acceptance, cost efficiency, and functional versatility. Their strong compatibility with spray-drying and emulsification processes, combined with excellent film-forming and protective properties, makes them highly suitable for large-scale food manufacturing.

Aligned with clean-label, plant-based, and natural ingredient trends, polysaccharides are extensively used in encapsulating vitamins, minerals, flavors, and nutraceuticals across functional food and beverage applications. Strong agricultural supply chains in the region ensure reliable raw material availability and economic scalability. Their ability to protect sensitive actives from heat, moisture, and oxidation positions polysaccharides as the preferred shell material in the Asia Pacific food encapsulation market.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=245671954

China Emerges as the Largest Country-Level Market

China is estimated to be the largest country-level market in the Asia Pacific food encapsulation industry. Growth is driven by its advanced food processing infrastructure, large consumer base, and rising demand for fortified foods, dietary supplements, and infant nutrition products. Increasing health awareness, micronutrient deficiencies, and strong government-backed nutrition initiatives continue to stimulate demand for encapsulated ingredients.

With substantial investment in food technology innovation, manufacturing modernization, and regulatory alignment, China remains a focal point for encapsulation deployment. International ingredient suppliers continue to expand local manufacturing, R&D capabilities, and regulatory integration under frameworks governed by the National Medical Products Administration (NMPA). High domestic consumption, export-driven functional food production, and government-supported nutrition programs reinforce China’s leadership position in the regional market.

Leading Asia Pacific Food Encapsulation Companies:

The report profiles key players such as Yakult Honsha Co., Ltd. (Japan), Danone (France), Nestlé (Switzerland), Morinaga Milk Industry Co., Ltd. (Japan), Inner Mongolia Yili Industrial Group (China), Mengniu Dairy (China), By-Health Co., Ltd. (China), Meiji Holdings (Japan), Fonterra Co-operative Group (New Zealand), Amul (India), CJ CheilJedang (South Korea), and Sanzyme Biologics Pvt. Ltd. (India).