“Innovations & Developments in plant-based protein augmenting the vegan trend, which in turn driving the market for plant-based protein.”

The global plant-based protein market size is projected to grow from USD 10.3billion in 2020 to USD 14.5billion by 2025, in terms of value, recording a compound annual growth rate (CAGR) of 7.1% during the forecast period. Some of the major factors driving the growth of theplant-based proteinmarket include growing demand in the food industry, increasing demand for pea-based protein, and the opportunity to expand in the high growth potential markets.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=225613386

“The foodsegmentis projected to dominate the plant-based protein market throughout the forecast period.”

The food segment is projected to dominate the plant-based protein market, by application, in terms of value,due to their extensive use in human nutrition.Plant-based proteinis incorporated in food to add nutritional value to various food products. Different product sources are developed into types such as isolates, concentrates, and even textured proteins, which can be utilized in different types of plant-based foods, including dairy and meat alternatives, ready meals, confectionery, and other food types.

“The liquidsegment is projected to grow at the highest growth rate during the forecast period.”

The liquid segment is projected to grow at the highest growth rate due to its major use in plant-based dairy, food & beverages, and nutritional supplements such as shakes and other healthy beverages. Wet/liquid form of processing is a mainstream technology used for producing plant-derived protein isolates. This form of processing involves the consumption of copious amounts of water and energy. During the extraction of the protein, the source crop is dispersed in water so that other components, such as carbohydrates, are also extracted through ultrafiltration or iso-electric precipitation. With the growing demand for plant-based protein in the food and feed segments, the demand for plant-based protein that is obtained through wet processing is projected to remain high during the forecast period.

Request for Customization: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=225613386

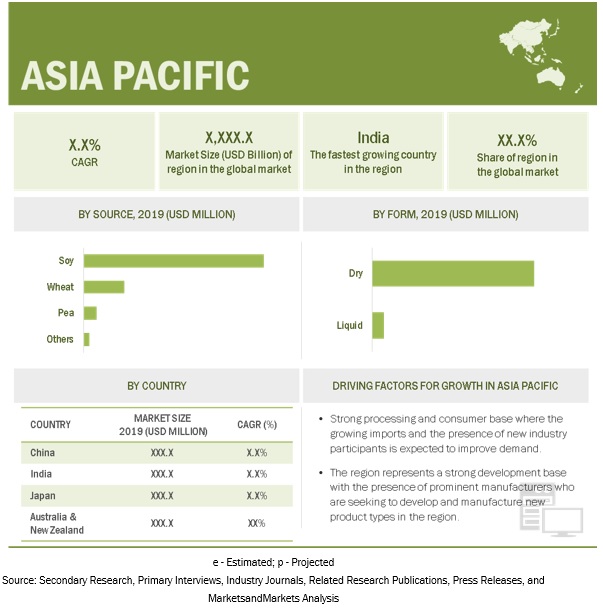

“Asia Pacificis projected to record the highest growth during the forecast period.”

The Asia Pacificregion is projected to record the highest growth during the forecast period. The risingvegan food consumption has led to anincreased demandfor plant-based food. The feed sector is also growing in countries such as China, India, and Japan, which aids the growth of the plant-based marketin the region.Some of the leading players operating in the region include Herblink Biotech Corporation (China)and ET Chem (China). Apart from regional manufacturers, major foreign players such as Cargill(US), DSM (The Netherlands), and ADM (US)have established their production and research & development facilities in countries in the Asia Pacific region.

The plant-based protein marketcomprises major players,which includeDSM (Netherlands), ADM (US), DuPont (US), Kerry Group (Ireland), Cargill (US), Glanbia (Ireland), Wilmar International (Singapore), Emsland Group (Germany), Puris (US), Cosucra Group (Belgium), Batory Foods (US), Roquette Freres (France), Ingredion (US), BurconNutracience (Canada), Sotexpro (France), AGT Food & Ingredients (Canada), Beneo (Germany), ProlupinGmbh (Germany), Aminola (Netherlands), Herblink Biotech Corporation (China), ET Chem (China), Shandong Jianyuan Group (China), The Greenlans LLC (US), and Parabel (US)