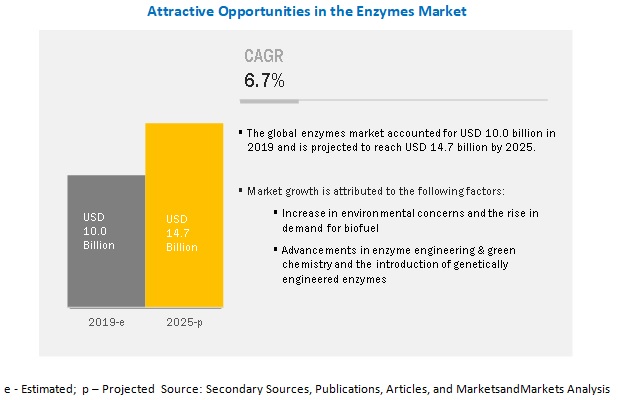

The report “Biofungicides Market by Type (Microbial species, Botanical), Mode of Application (Soil treatment, Foliar application, Seed treatment), Species (Bacillus, Trichoderma, Streptomyces, Pseudomonas), Crop Type, Formulation, and Region – Global Forecast to 2025″ The biofungicides market is estimated to account for USD 1.6 billion in 2020 and is projected to grow at a CAGR 16.1% from 2020, to reach a value of USD 3.4 billion by 2025. Factors such as an increase in demand for organic food products, stringent government regulations against the use of chemical-based crop protection products, and the growing health concerns associated with chemical-based products are projected to drive the growth of the market of biofungicides.

Download PDF brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=8734417

By type, the microbial segment is estimated to account for a larger market share, in terms of value, in 2020

Strains of microbial species are derived from bacteria, fungi, and viruses. Species, such as Bacillus, Trichoderma, and Pseudomonas, are majorly used to derive the active ingredients that are used as anti-fungal agents. Microbial biofungicides are proven to be efficient in controlling fungal pathogens without causing any harm to the host plant or the environment.

Trichoderma, on the basis of species, is estimated to hold the largest share in the biofungicides market, in terms of value, in 2020

Trichoderma has higher environmental diversity and tolerance to soil pH, changes in temperature, and moisture. The use of these strains also ensures lower instances of reapplication (once in 12 weeks) as opposed to bacterial strains (once in 4 weeks). However, Trichoderma-based commercial products are expensive and have a relatively lower shelf life as compared to Bacillus-based products, due to which the market for the latter is growing at the fastest rate during the forecast period

The soil-treatment segment, on the basis of mode of application, is estimated to hold the largest share in the biofungicides market, in terms of value, in 2020

Soil treatment is one of the most commonly adopted modes of application for biofungicides. This is mainly due to many fungal infestations in the soil/root zone of the plant. The majority of the biofungicides available in the market are used for the treatment of soil and root-zone diseases. Trichoderma-based products are widely distributed biofungicides across the globe and have a majority of the products available for treating soil and root zone diseases. However, in regions such as North America, South America, and Europe due to technological advancements, the market for biofungicides is projected to grow. The major players in the market are also investing significant amounts in R&D activities of biological seed treatment solutions, due to which seed treatment is projected to record the fastest growth rate during the forecast period.

By crop type, the fruits & vegetables segment is estimated to account for a larger market share, in terms of value, in 2020

The fruits & vegetables segment is projected to account for the largest share in the biofungicides market. A majority of the commercially available biofungicides products are fruits and vegetables. Key players in the market are introducing products, which would target pathogens in crops, such as berries, potatoes, tomatoes, bananas, and apples.

By form, the wettable powder segment in the biofungicides market is projected to account for the largest market share in 2020

The wettable powder segment accounts for the largest share in the market during the forecast period. Powder formulations can easily be mixed with basic or acidic solutions in a spray tank or in the irrigation line depending upon the prevailing soil requirements. Bacillus spp. is the most commonly used source of biofungicides and is readily available in powdered form. The powdered form is easy to produce on a commercial scale and provides farmers with various application choices. This ease of availability has made it a preferred form among growers across the globe.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=8734417

North America is projected to grow at the highest CAGR during the forecast period

North America accounted for the largest market share during the forecast period due to the presence of major players in the market in the region. The region witnesses the adoption of integrated pest management and organic farming practices, which has also promoted the growth of the market. The region is also one of the largest producers of fruits & vegetables. In addition, the increasing concerns about food safety across the globe have also contributed to the growth of the market.

This report includes a study on the marketing and development strategies, along with a survey of the product portfolios of the leading companies operating in the biofungicides market. It includes the profiles of leading companies, such as BASF SE (Germany), Bayer AG (Germany), Syngenta AG (Switzerland), FMC Corporation (US), Nufarm (Australia), Novozymes (Denmark), Marrone Bio Innovations (US), Koppert Biological Systems (Netherlands), Isagro S.P.A (Italy), T. Stanes & Company Limited (India), BioWorks (US), The Stockton Group (Israel), Valent Biosciences (US), Agri Life (India), Certis U.S.A (US), Andermatt Biocontrol AG (Switzerland), Lesaffre (France), Rizobacter (Argentina), Vegalab S.A (US), Biobest Group NV (Belgium), and Biolchim (Italy).

About MarketsandMarkets™

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies’ revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the “Growth Engagement Model – GEM”. The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write “Attack, avoid and defend” strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets’s flagship competitive intelligence and market research platform, “Knowledgestore” connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Aashish Mehra

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

sales@marketsandmarkets.com