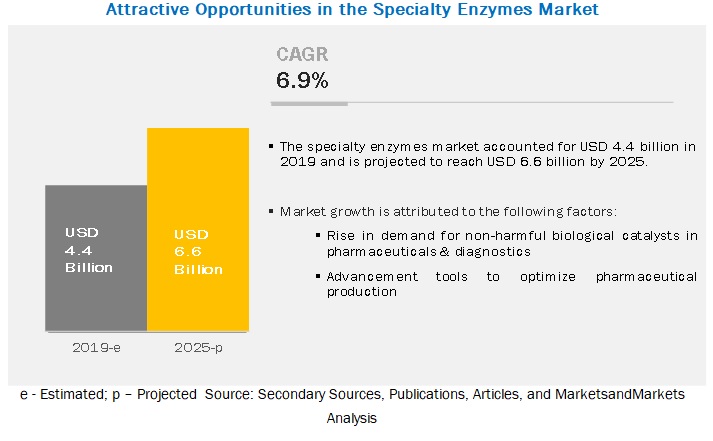

According to MarketsandMarkets, the specialty enzymes market is estimated to be valued at USD 4.4 billion in 2019 and is projected to reach USD 6.6 billion by 2025, recording a CAGR of 6.9% in terms of value. Due to the rise in demand for non-harmful biological catalysts in pharmaceuticals & diagnostics and advancement tools to optimize pharmaceutical production, specialty enzymes market has been boosting. These factors are projected to drive the growth for the specialty enzymesmarket during the forecast period.

Enzymes play an important role as a biological catalyst in the processing for several applications such as pharmaceutical, research &biotechnology, and diagnostics. In addition, enzymes are increasingly used as a substitute for chemical catalysts, which is significantly contributing to the growth of the specialty enzymesmarket.Developments such as protein engineering and genetic engineering provide scope for research & development in enzymes. The research and development activities help the industry to innovate products and meet the demand of industries by increasing production.In addition, biotechnology will help in increasing the efficiency of enzyme production and enhance its properties.Along with this, the increase in demand for diagnostics for the treatment of various chronic diseases is also contributing to the growth of the specialty enzymes market. Enzymes, such as polymerases & nucleases and carbohydrases, are used for the production of pharmaceuticals.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=21682828

In terms of type, the polymerases & nucleases segmenthas shown significant growth in the market due to its wide range of usesacross various applications.The core structure and properties of polymerases are highly conserved through evolutions, as they function in coordination with several other proteins in order to synthesize nucleic acids in an accurate, efficient, and well-regulated manner. The ability of specialty enzymes to catalyze chemical reactions and increase its applications hascontributed to the growth of the specialty enzymes market.In addition, enzymes have several other benefits,such as lower production costs, higher product quality, reduced power energy consumption, and less wastage. These factors also drive the growth of the specialty enzymes market, while the use of specialty enzymes in pharmaceuticals is increasing for the production of drugs.

Asia Pacific is projected to witness the fastest growth in the specialty enzymes market during the forecast period due to the globalization of business and technological innovations. The Rest of the World (RoW) enzymes market has been growing due to advancements in various specialty applications and a rise in demand in developed countries. Novozymes (Denmark) expands its research &development facilities in Brazil that would focus on biotechnology-based innovations and developments in new enzyme product offerings. In addition, enzymes are being used increasingly to optimize the pharmaceutical industry. One of the major factors contributing to the growth of the enzymes market in the Asia Pacific and Rest of the World (RoW)regions is the increase in population in this region, which is driving the growth of the pharmaceutical and diagnostics industries.These factors are the major factors driving the market growth for enzymes in the Asia Pacific and Rest of the World (RoW) region for specialty applications.